RTL loan underwriting is document-heavy, repetitive, and highly sensitive to missed details. A single loan package may contain anywhere from 100 to 1,000 pages, and every page matters. Underwriters must review appraisal reports, title documents, bank statements, contractor budgets, insurance records, and other materials against internal checklists and investor guidelines before making a lending decision.

For private lenders, that process often takes one to two hours per package. When teams are handling multiple submissions each day, manual review quickly becomes a bottleneck.

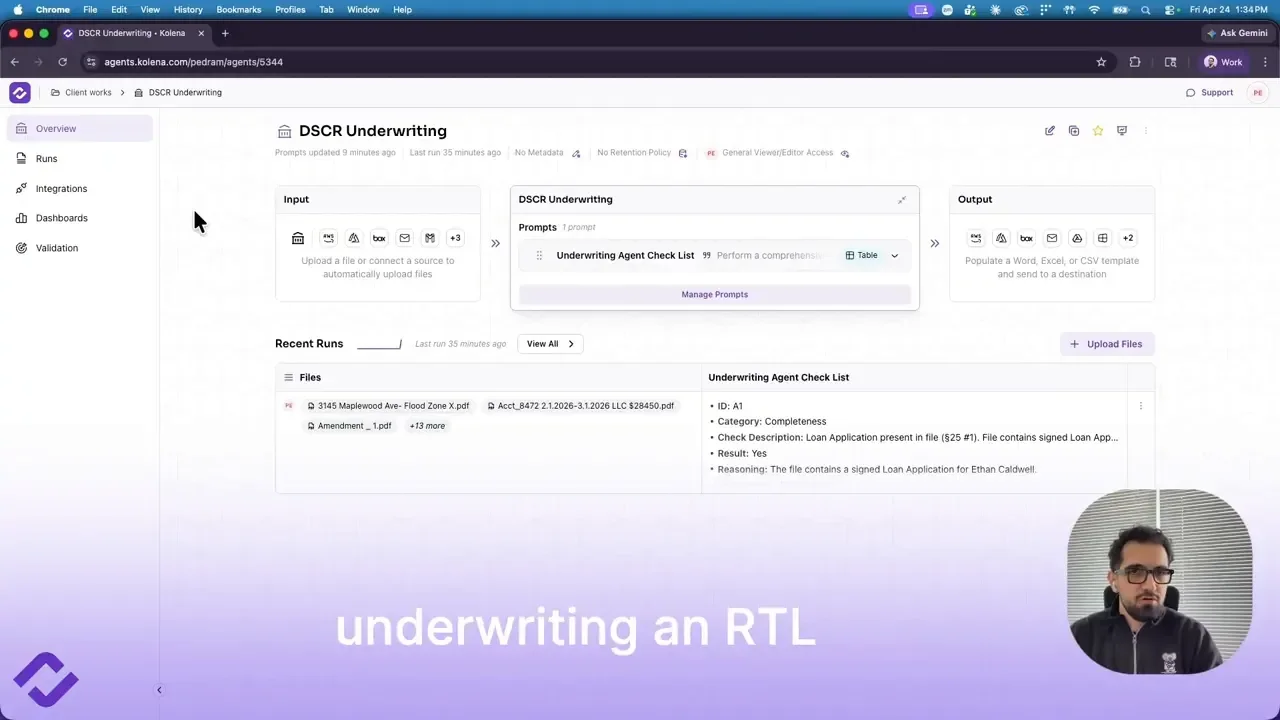

AI underwriting tools are now changing that equation. By applying a structured checklist across all uploaded documents at once, AI can reduce underwriting time by roughly 95 percent while preserving the core discipline of document validation and guideline compliance. In the example covered here, an AI agent processes a full RTL loan package in about five minutes, runs more than 100 checks, flags missing items, and generates a clear recommendation on whether the loan should move forward.

Why RTL underwriting takes so long

The challenge with residential transitional lending, or RTL, is not just the number of documents. It is the fact that the information needed for an underwriting decision is scattered across many formats, issuers, and templates.

A lender might need to confirm:

Whether bank statements are complete and consecutive

Whether title-related documentation is present

Whether insurance requirements are satisfied

Whether the contractor budget aligns with the deal structure

Whether the package meets a specific investor’s eligibility criteria

These checks are rarely isolated. Underwriters must compare what is in the file against a formal checklist and then validate the package against investor-specific rules. That means even experienced teams still spend significant time hunting for information, cross-referencing guidelines, and documenting exceptions.

The result is a process that is important, but slow.

What AI underwriting automates

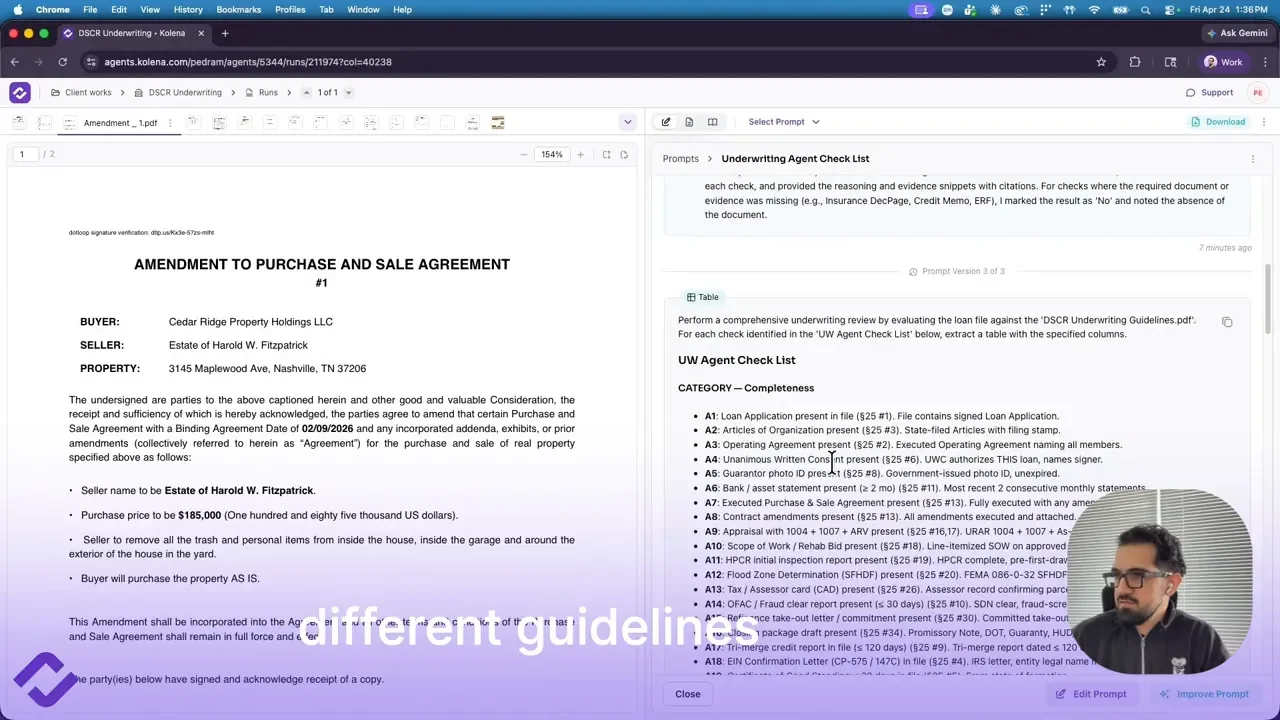

The AI workflow demonstrated here centers on a simple but practical concept: load the loan package into an agent, give the agent a checklist, attach the relevant investor guideline, and let the system perform the review.

Instead of manually opening each file and checking it line by line, the AI agent processes the entire package simultaneously. It extracts information from multiple document types, identifies relevant fields, and returns structured results for each underwriting rule.

In this setup, the system can:

Review large RTL or DSCR loan packages

Process documents from different banks and providers

Apply more than 100 underwriting checks in one run

Return a pass, warn, or fail result for each check

Explain why an item passed or failed

Generate an executive summary with a recommendation

This matters because automation is only useful if it produces actionable output. A list of extracted fields is not enough. Underwriters need a decision-ready review that highlights missing documents, identifies compliance gaps, and supports next steps.

How the document review works in practice

In the example loan package, 16 documents are uploaded to the AI agent. Those documents come in different shapes and formats, including bank statements and other underwriting records that typically vary by institution.

That variability is one of the biggest barriers to automation in lending. Different banks structure statements differently. Title and insurance documents may come from different systems. Some files are highly standardized, while others are not.

The AI agent is designed to handle this inconsistency by extracting information across sources without requiring every document to follow the same template. Once the documents are loaded, a single prompt instructs the system to run the full underwriting checklist and compare the findings against the relevant guideline.

This turns a fragmented package into a structured review process.

The checklist is the engine

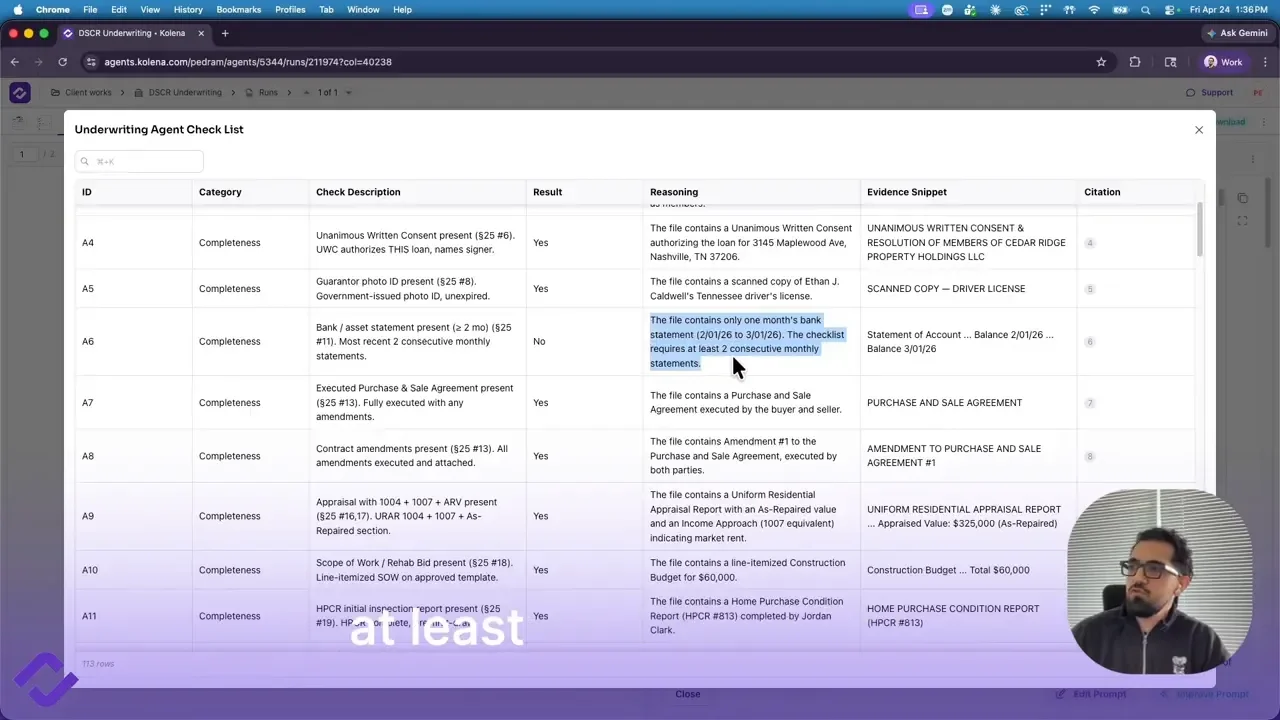

The core of the workflow is the underwriting checklist. In the demonstration, 113 separate checks are applied to the package. Those checks are used to verify whether required documents are present, whether data points satisfy the rule being tested, and whether the package is aligned with lending requirements.

Each result is returned in a clear format. If something is missing or incomplete, the system does not stop at a generic failure. It explains the reason.

That level of specificity is critical for remediation. If a package is not ready to approve, the underwriter needs to know whether to request additional statements, ask for insurance documentation, or escalate another issue before moving forward.

Examples of the issues AI can flag

The demonstration includes several concrete examples of how the AI agent identifies problems in an RTL loan package.

One flagged issue involves bank statements. The checklist requires at least two consecutive monthly statements, but the file contains only one month. The system marks that check as failed and explains why.

Other missing items include:

No CPL provider information in the file

No hazard insurance documentation provided

These are exactly the kinds of issues that can delay a file or lead to a poor decision if overlooked during manual review. By surfacing them automatically, the system helps teams move from document collection to exception management.

That is an important shift. Instead of spending most of their time searching for missing items, underwriters can focus on assessing the significance of the exceptions and deciding what to do next.

Investor guidelines can be built into the review

One of the strongest features of the workflow is the ability to attach investor guidelines directly to the agent’s instructions. This is especially valuable for lenders who sell or structure loans according to different investor matrices, requirements, or overlays.

Rather than applying a generic checklist in isolation, the agent can use the relevant guideline while evaluating the package. In practice, that means the system is not just asking whether a document exists. It is asking whether the contents of the file satisfy the specific standard required by the investor.

This approach offers two advantages:

Consistency: every file is reviewed against the same criteria

Scalability: multiple investor programs can be supported without recreating the process from scratch

For lenders managing multiple capital partners, this can significantly reduce operational friction. A process that once had to be repeated manually for each investor can instead be standardized and replicated through the AI agent.

From checklist results to a lending recommendation

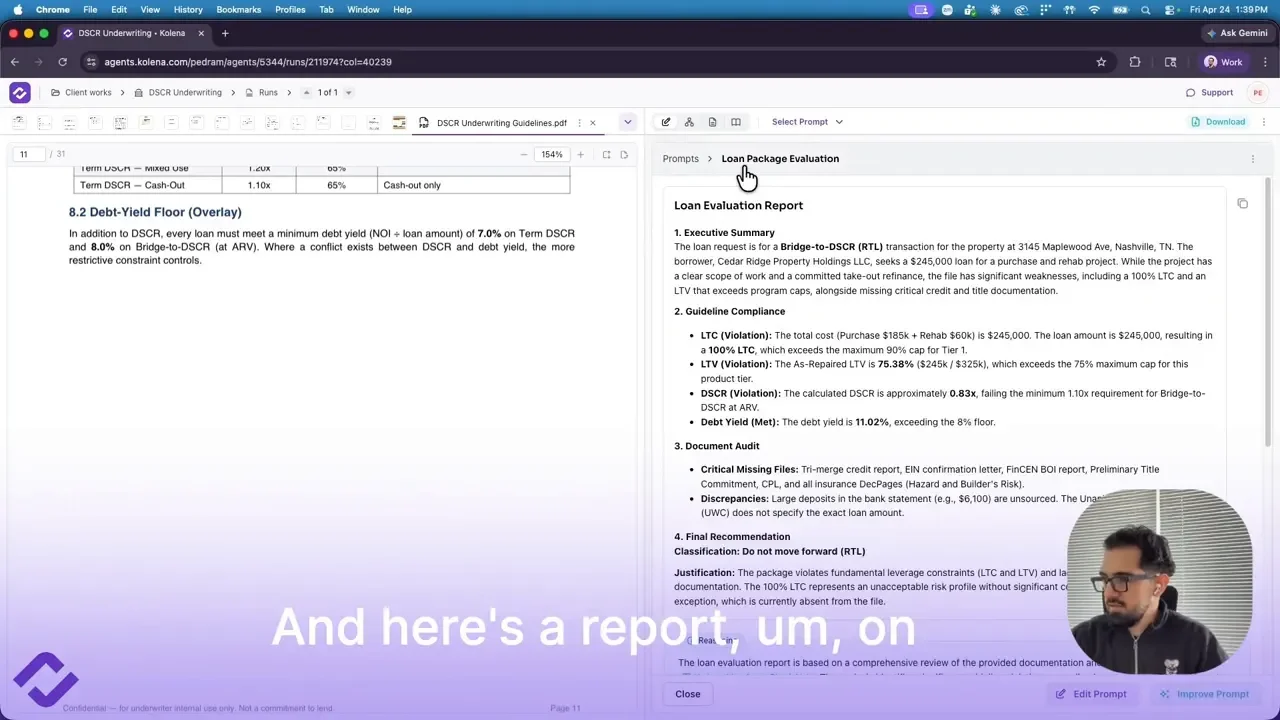

Checklist automation becomes even more useful when it feeds directly into reporting. After running the checks, the agent can generate a concise underwriting summary that answers the most important operational question: should this loan move forward?

In the example, the AI produces an executive summary that identifies the loan as an RTL request seeking $245,000 and uses the 113 checklist points as the basis for its recommendation. The final determination is straightforward: do not move forward.

That conclusion is not presented as a black box. It is supported by the missing and failed requirements identified earlier in the review.

This kind of summary can help teams:

Speed up internal decision-making

Create a clean handoff between operations and credit teams

Document why a file was paused or declined

Standardize communication across underwriting workflows

The same workflow can support DSCR loans

Although the example focuses on RTL underwriting, the same approach can be used for DSCR loans as well. The process does not fundamentally change. What changes is the guideline and checklist being applied.

That is a meaningful point for lenders looking to scale automation across product lines. If the platform can ingest documents, follow instructions, and apply the right rules, then the underlying workflow remains stable even when the lending program changes.

In other words, the value is not limited to one loan type. The broader opportunity is to create a repeatable AI underwriting framework that can support multiple credit products with the appropriate controls.

What a 95 percent reduction in underwriting time really means

A reduction from one to two hours down to roughly five minutes per package is more than a productivity improvement. It changes how an underwriting operation can function.

At that level of efficiency, teams can:

Review far more packages in the same amount of time

Reduce turnaround times for borrowers and brokers

Improve consistency across reviewers

Spend more time on judgment and exception handling

Scale lending operations without linearly scaling headcount

For private lenders, these benefits are especially relevant. Volume can be uneven, document quality varies widely, and investor requirements are often strict. AI does not remove the need for underwriting discipline. It strengthens it by making the first layer of review faster, more systematic, and easier to document.

Why this matters for modern lending operations

The larger takeaway is that AI underwriting works best when it is grounded in real workflows. The most useful systems are not abstract assistants. They are operational tools that can read the actual loan package, apply the actual checklist, and produce results that fit the way lenders already make decisions.

That is the practical value demonstrated here. A loan package is uploaded. The agent reads every document. More than 100 checks are applied. Missing items are flagged with reasons. Investor guidelines are consulted. A recommendation is generated.

What previously required one to two hours of manual review can be completed in about five minutes.

For organizations evaluating ways to modernize underwriting operations, that combination of speed, structure, and explainability is likely to be the real differentiator. More information about the platform behind this workflow is available on Kolena’s website.