Banking compliance sounds straightforward until you are the person responsible for proving that every credit card statement includes the right disclosures, in the right format, every single time. In most banks and credit unions, that still means pulling up a statement template, opening the CFPB rulebook, finding the relevant clauses, and manually checking line by line.

The problem is that this work is never really finished. Different card products have different statement templates. Those templates change with promotions, seasonal campaigns, redesigns, and layout updates. What looks like a small visual tweak can create real compliance risk.

That is where automated banking compliance becomes a lot more than a productivity upgrade. It becomes a way to get consistent, repeatable, defensible reviews without relying on sampling or exhausting your team.

Why manual statement reviews break down

Credit card statement compliance is one of those workflows that appears manageable until volume and variation kick in. A team may be able to review one template manually. But most institutions are juggling multiple products, frequent template changes, and ongoing pressure to reduce operational risk.

Manual reviews create a few obvious problems:

They are slow. Every review requires opening source documents, locating requirements, and comparing them against the statement.

They are repetitive. Teams keep rechecking similar issues every time a template changes.

They do not scale. More products and more statement variants mean more complexity.

They are vulnerable to human error. People miss things, especially after hours of checklist work.

For banking compliance teams, this is not just an efficiency issue. It is a coverage issue. If your process only allows you to inspect a tiny sample of statements, you are accepting a blind spot by design.

That is especially risky in a regulatory environment where the CFPB's Regulation Z sets clear expectations for credit card disclosures and where enforcement consequences are real.

What automated CFPB statement review actually does

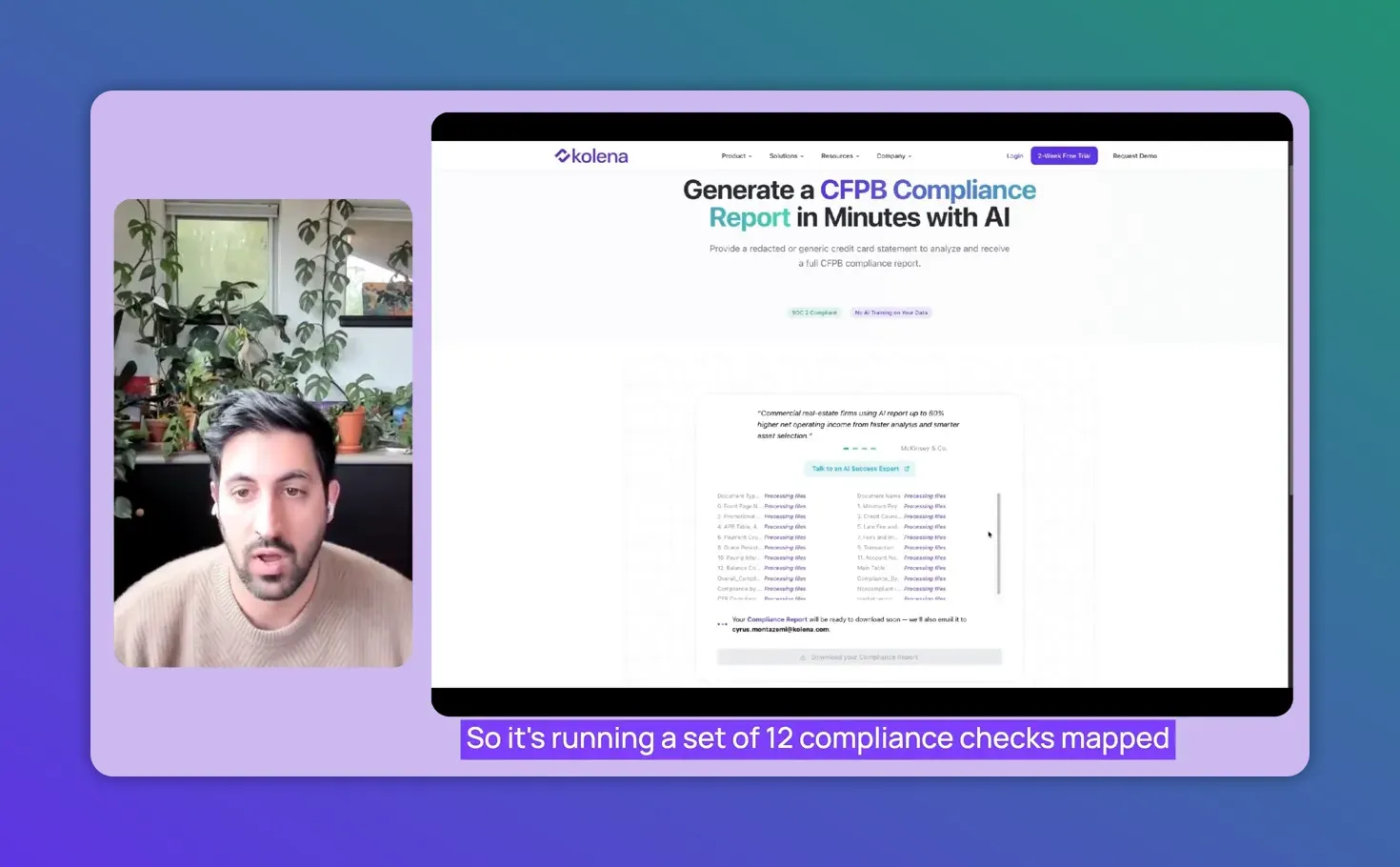

A modern compliance agent changes the workflow from manual comparison to structured analysis. Instead of reading a statement and hunting through rules by hand, you upload the credit card statement, enter a work email, and the system runs a set of mapped checks automatically.

In this case, the process runs 12 compliance checks aligned to CFPB requirements. The output is not just a pass or fail. It is a clear compliance report that shows:

What is compliant

What is not compliant

Why each determination was made

What part of the document needs attention

What next steps are recommended

That last piece matters. Good banking compliance software should not stop at flagging an issue. It should help the team move from detection to action.

If you want a practical example of that kind of workflow, Kolena offers a free AI-Powered CFPB Compliance Test that lets teams upload a statement and receive a report with detailed findings.

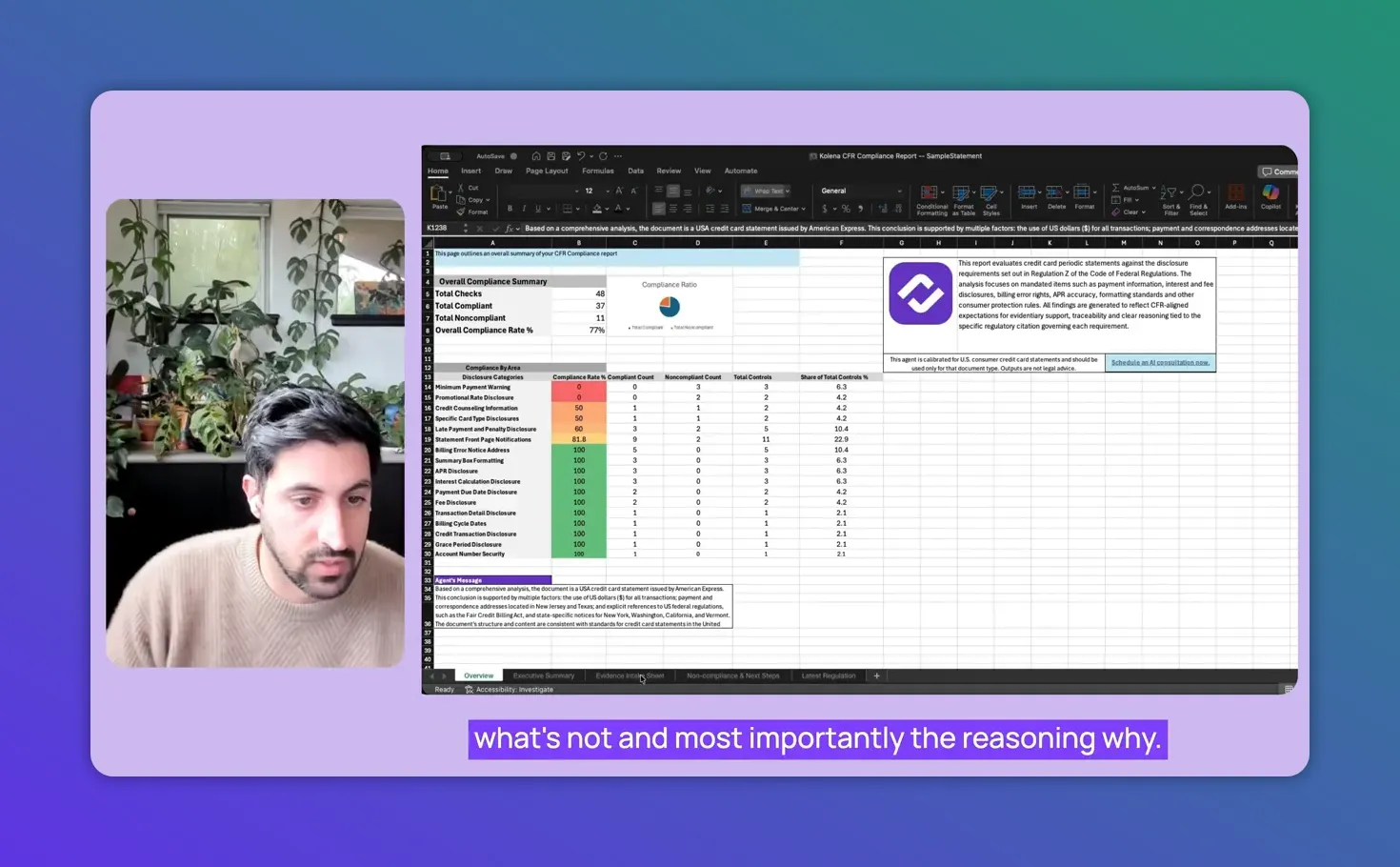

What a useful compliance report should include

A compliance report needs to do more than summarize results. It has to be usable by compliance, legal, audit, and operations teams. The most effective reports include three layers of information.

1. Executive summary

The executive summary gives a fast overview of the areas that need attention. This is where leaders can quickly understand whether the statement is broadly aligned or whether there are material issues to address before distribution.

2. Requirement-level results

Each reference code should link to a specific requirement and show its compliance status. Ideally, the report also indicates a compliance percentage or scoring view so teams can prioritize fixes.

3. Recommended actions

Findings are most valuable when they come with suggested next steps. That makes it easier to distribute remediation across design, operations, compliance, or legal teams without forcing everyone to reinterpret the result from scratch.

This is one of the biggest gains in automated banking compliance. Instead of generating more work for the team, the review process creates a cleaner handoff for remediation.

Why auditability matters as much as accuracy

Many AI tools can extract information from documents. That alone is not enough for regulated workflows.

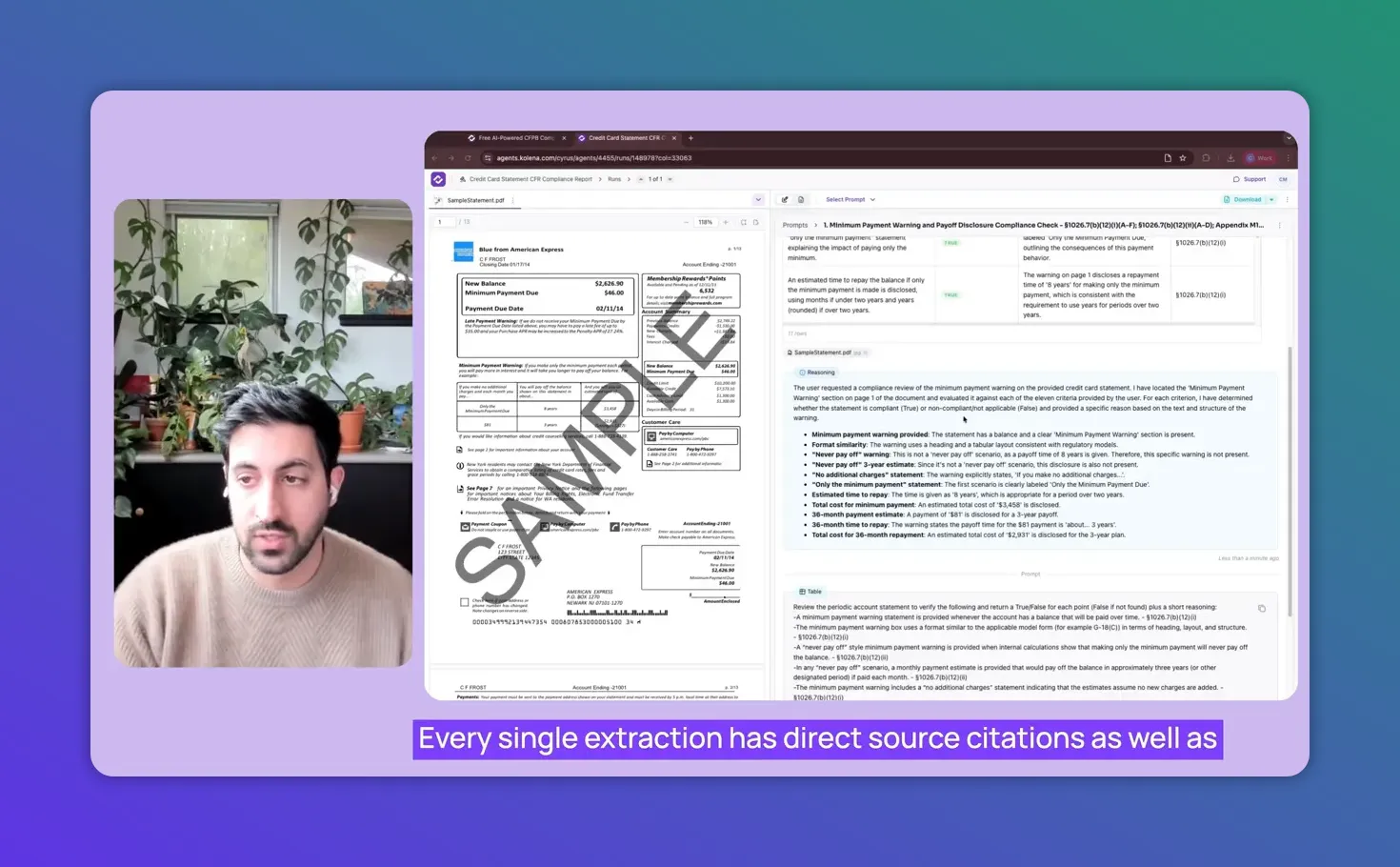

In compliance, the real question is not just whether the system found something. It is whether the system can show how it found it and why it reached the conclusion it did.

That is why the best systems do more than read uploaded data. They cross-reference extracted information against internal business rules and external regulatory requirements, such as Regulation Z. They also preserve the reasoning used in each decision.

When this is done well, every extraction includes:

Direct source citations tied to the document

Reasoning for why the selected data was chosen

Business logic where inference is required

Traceability back to the original source material

That is a very different standard from a black-box system that returns an answer with no explanation. In regulated banking compliance, an audit trail is not a nice-to-have. It is the difference between a result that can stand up to scrutiny and one that cannot.

Kolena describes this approach as decision-grade AI, which is a useful phrase because it captures the real bar for financial services. The output must be good enough to support decisions, reviews, and audits, not just experimentation.

For teams evaluating tools in this category, the right benchmark is simple: can the system show the source, the logic, and the reason for every finding?

The real cost of staying manual

Manual review processes feel familiar, but they come with hidden costs that compound over time.

Industry data cited here points to manual reconciliation being roughly 23% prone to non-compliance errors. At the same time, the CFPB has ordered more than $19 billion in consumer relief to date. Those numbers make one thing clear. Sampling is no longer an adequate strategy for high-stakes consumer finance operations.

Many manual teams reportedly audit only about 1% of statements. That leaves a massive gap between what is shipped and what is actually reviewed. If a disclosure issue sits outside the sample, the process may never catch it.

Automated banking compliance changes that equation by moving from sample-based review to complete coverage. According to the workflow described here, the system can provide:

100% coverage of statements under review

Up to 80% less manual effort

Improved detection of issues people often miss during repetitive review work

That does not just save time. It reduces operational risk while giving teams a repeatable process they can rerun whenever a statement template changes.

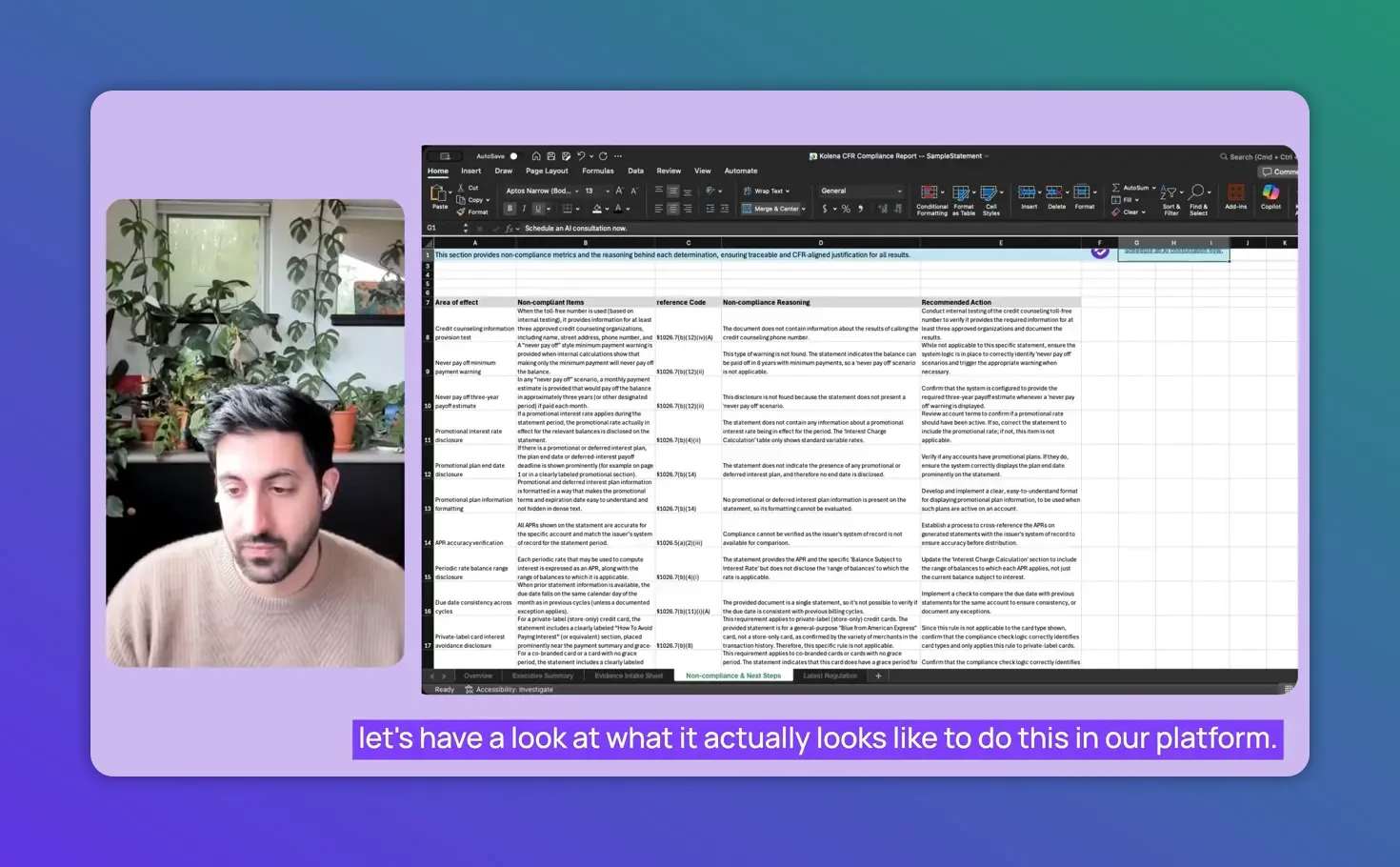

What the workflow looks like in practice

The practical flow is refreshingly simple.

Upload a credit card statement.

The system processes the document and extracts relevant sections and fields.

It applies compliance checks mapped to CFPB requirements and business logic.

A report is generated and sent by email, with a downloadable version available in the platform.

Teams review findings, inspect citations, and act on recommended next steps.

Under the hood, the system is doing much more than OCR or keyword matching. It is evaluating document segments, tying them to rules, and preserving the reasoning chain. That is what makes it suitable for banking compliance rather than generic document processing.

For organizations exploring broader use cases beyond statement review, Kolena also has a page on consumer banking compliance testing that outlines how AI testing can support regulatory adherence across workflows.

What to look for in a compliance automation platform

If you are considering automation for statement review, there are a few capabilities worth insisting on.

Requirement mapping: Checks should align directly to relevant CFPB or Regulation Z obligations.

Source-cited findings: Every result should point back to the originating document evidence.

Reasoning visibility: Teams should be able to inspect the logic behind the result.

Actionable reporting: Findings should include recommendations, not just flags.

Repeatability: The review should be easy to rerun whenever templates change.

If a tool can do all five, it has a real chance of improving both speed and confidence in your banking compliance process.

For a closer look at the specific statement review workflow, the Automate CFPB Credit Card Statement Compliance Reviews resource is a relevant next read.

From checklist work to continuous assurance

The biggest shift here is not just automation. It is mindset.

Manual statement review treats compliance like a periodic checklist exercise. Automated banking compliance turns it into a repeatable assurance process. Every time a template changes, the same checks can run again. Every result comes with evidence. Every issue is documented with reasoning and next steps.

That means less time flipping through rulebooks and more time improving the quality of the process itself.

For banks and credit unions managing credit card portfolios, that is a meaningful upgrade. It reduces blind spots, lowers manual burden, and creates an audit trail that teams can actually defend.

The old model is sampling your risk. The better model is automating your certainty.