What Is Banking Compliance Automation?

Banking compliance automation embeds regulatory rules directly into daily operations, replacing manual reviews with real-time risk monitoring, automated Know Your Customer (KYC) checks, and instant regulatory reporting. It cuts costs, minimizes human error, and instantly generates auditable trails for regulators.

Key use cases:

Document management: Automatically enforces compliance rules and embeds correct disclosures during document creation.

Loan package review and validation: Automatically verifies document completeness, validates borrower and loan data across files, and flags missing information or inconsistencies before underwriting.

UCC filing review automation: Automatically extracts and validates UCC filing information, identifies errors, and tracks renewal deadlines to help maintain secured lending compliance.

Due diligence and risk management workflows: Automates background checks, risk assessments, and compliance reviews to support consistent and scalable due diligence processes.

This is part of a series of articles about AI for Finance

In this article:

Why Banks Are Automating Compliance

Rising Compliance Costs and Operational Pressure

The cost of regulatory compliance has been increasing for banks worldwide, driven by evolving regulations and heightened scrutiny from regulators. Manual compliance processes require significant staffing, extensive training, and continual updates to keep up with regulatory changes. As a result, compliance departments face pressure to do more with less, leading to bottlenecks, backlogs, and increased risk of non-compliance.

How automation helps:

Automation reduces the need for manual intervention in routine compliance activities. Automated systems can process large amounts of data, flag inconsistencies, and generate reports faster than human teams. This lowers operational costs and allows banks to redeploy compliance staff to higher-value tasks, such as investigating complex cases or developing new risk controls.

Faster Onboarding and Better Customer Experience

Customer onboarding in banking is a regulated process, involving identity verification, anti-money laundering (AML) checks, and extensive documentation. Manual onboarding is often slow, causing frustration for customers and increasing the risk of drop-offs.

How automation helps:

Compliance automation accelerates onboarding by automating document collection, verification, and background checks, allowing banks to approve new accounts more quickly. A faster onboarding process makes it easier for clients to access banking services without unnecessary delays. Automated compliance checks also reduce errors and inconsistencies that can lead to compliance breaches or customer dissatisfaction. As a result, banks can attract and retain more customers while maintaining compliance standards.

Better Audit Readiness

Maintaining audit readiness is a constant challenge for banks, given the volume and complexity of compliance documentation required by regulators. Manual record-keeping can result in missing, incomplete, or inconsistent documentation, increasing the risk of audit findings or penalties.

How automation helps:

Compliance automation ensures that all actions, decisions, and documentation are captured and stored in a centralized, searchable repository. With automated audit trails and reporting capabilities, banks can respond to audit requests promptly. These systems provide evidence of compliance activities, making it easier to demonstrate adherence to regulatory requirements. This reduces the stress and resource drain of audit cycles and helps banks maintain a proactive stance toward regulatory oversight.

Stronger Financial Crime Detection

Financial crime, including money laundering, fraud, and terrorist financing, is a persistent threat to banks. Traditional monitoring methods rely on manual review of transactions and customer behavior, which can be slow and ineffective at detecting complex schemes.

How automation helps:

Compliance automation uses AI and analytics to monitor transactions in real time, identify unusual patterns, and trigger alerts for investigation. Automated systems can analyze large datasets across multiple channels, detecting red flags that might be missed by human analysts. By strengthening financial crime detection, banks can reduce losses, prevent reputational damage, and fulfill regulatory obligations.

Banking Compliance Automation Use Cases

1. Document Management

Document management is a core area where compliance automation delivers value. Banks handle large volumes of documents daily, including customer records, loan agreements, and regulatory forms. Manual document management is prone to errors such as misfiling, lost paperwork, and inconsistent versioning, which can result in compliance breaches and audit issues.

Automation platforms digitize documents, extract key data, and organize files according to regulatory requirements, ensuring consistency and easy retrieval. Automated document management systems enhance security and access control. These platforms enforce permissions, monitor document usage, and maintain logs of interactions with sensitive files. As a result, banks can protect customer data, ensure privacy compliance, and produce required documentation during audits or regulatory reviews.

2. Loan Package Review and Validation

Loan origination involves the collection and validation of numerous documents, credit reports, and regulatory disclosures. Manual review of loan packages is time-consuming and increases the risk of missing documents or inconsistent data entry. Automation simplifies this process by validating document completeness, cross-referencing data points, and flagging discrepancies or missing information.

By automating loan package review, banks can accelerate approvals while maintaining compliance with lending regulations. Automated workflows ensure that each loan file meets regulatory standards before approval, reducing rework and the risk of non-compliance. This shortens turnaround times for customers and improves the reliability of lending operations.

3. UCC Filing Review Automation

Uniform Commercial Code (UCC) filings are critical for securing interests in collateral during commercial lending. Reviewing UCC filings manually requires checking multiple details across various documents and databases, making the process slow and error-prone. Automation can extract, compare, and validate UCC filing data, ensuring that required information is present and accurate before filings are submitted or renewed.

Automated UCC review reduces the risk of filing errors that could compromise a bank’s security interests or expose it to legal disputes. These systems can also track renewal dates and send alerts for necessary actions, helping banks maintain compliance with UCC requirements.

4. Due Diligence and Risk Management Workflows

Due diligence is central to banking compliance, especially during customer onboarding, loan origination, and ongoing risk monitoring. Manual due diligence processes often involve repetitive data collection, background checks, and risk assessments, which can slow operations and introduce inconsistencies. Automation simplifies these workflows by integrating data sources, automating background checks, and standardizing risk scoring.

Automated due diligence workflows improve accuracy and consistency. By centralizing risk data and automating decision rules, banks can identify high-risk customers or transactions and escalate them for review. This reduces the risk of regulatory breaches and supports informed decision-making.

Core Technologies Behind Banking Compliance Automation

AI Agents for Extracting, Validating, and Acting on Document Insights

AI agents are central to compliance automation, enabling banks to extract structured data from unstructured documents such as contracts, forms, and customer records. Using techniques such as natural language processing (NLP) and optical character recognition (OCR), these agents identify relevant information, validate its accuracy against internal and external databases, and flag inconsistencies or missing data. This reduces manual data entry and human error.

Beyond extraction and validation, AI agents can trigger automated actions based on document insights. For example, if a loan document is missing a required signature, the system can request completion or escalate the issue for review. These capabilities reduce turnaround times and ensure that regulatory requirements are met.

Workflow Automation for Approvals, Exceptions, and Escalations

Workflow automation manages compliance processes that require multiple approvals, exception handling, and escalations. Automated workflows define rules and routing paths, ensuring that compliance tasks are completed in the correct sequence and by the appropriate personnel. This reduces delays and provides transparency across the compliance lifecycle.

When exceptions or issues arise, such as missing documentation or unusual transaction patterns, workflow systems can escalate the matter to compliance officers. This maintains a clear audit trail of all actions taken. By automating these processes, banks can handle higher volumes of compliance activities while maintaining control and accountability.

Automated Data Validation and Anomaly Detection

Automated data validation tools ensure that information collected and processed by banks meets regulatory standards and internal policies. These tools cross-check data across multiple sources, flag discrepancies, and prevent errors from propagating through the system. As regulations become more stringent, automated validation helps banks stay compliant without slowing operations.

Anomaly detection uses machine learning to identify patterns or behaviors that deviate from the norm, such as unusual transaction volumes or suspicious account activity. By flagging these anomalies, banks can respond quickly to potential compliance breaches or financial crimes.

Integrations with Banking, Document, CRM, and Data Systems

Effective compliance automation requires integration with existing banking systems, document management platforms, customer relationship management (CRM) tools, and external data sources. These integrations allow automated compliance processes to access and update data in real time, ensuring that information is accurate and up to date across the organization. APIs and middleware enable these connections.

Integrated compliance systems reduce manual data transfers and minimize the risk of inconsistencies or data silos. By connecting compliance automation tools to core banking, CRM, and document repositories, banks can support end-to-end process automation, real-time reporting, and faster response to regulatory changes.

Related articles: ai earnings call analysis and ai portfolio monitoring.

Notable Banking Compliance Automation Tools

The market for banking compliance automation spans several categories of software. Some platforms focus on reading and acting on documents used in compliance work; others specialize in detecting financial crime and monitoring transactions; and others provide the governance and regulatory-management backbone that ties compliance programs together. The tools below are grouped into these three categories, with document-automation platforms covered first because they map most directly to use cases such as loan package review, UCC filing review, and due diligence.

AI Document Automation and Intelligent Document Processing

These platforms automate the capture, validation, and processing of documents used in compliance, lending, and onboarding workflows. They turn unstructured paperwork into structured, reviewable data and route it into downstream systems.

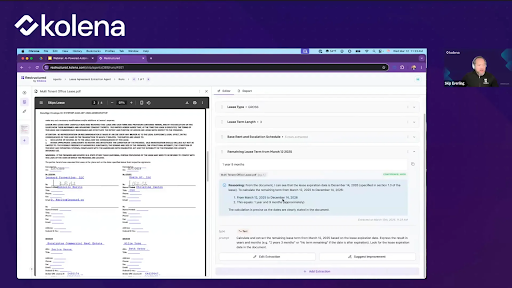

1. Kolena

Kolena is an AI-powered document workflow automation platform built for banks and financial institutions that handle high volumes of complex documents. It uses AI agents to read, validate, and act on unstructured documents such as regulatory filings, loan packages, leases, and policy files, turning manual review into automated workflows. For banking compliance, Kolena automates regulatory review, compliance testing, UCC filing review, and loan package review, and produces structured outputs that can feed downstream systems.

Key features include:

Specialized AI agents for compliance documents: Kolena includes agents oriented to underwriting analysis, compliance reviews, regulatory document processing, loan packet review, and policy checks. Each agent extracts required data points, validates them, and can trigger follow-on actions.

Extraction with reasoning, citations, and confidence scores: Every extracted field includes an explanation, a citation linking to the source document, and a confidence score.

Regulatory review, compliance testing, and UCC filing review: Workflows cover regulatory review, consumer banking compliance testing, UCC filing analysis, and loan package review. Kolena validates forms, cross-references documents, and flags inconsistencies or missing items.

Document handling across formats: Kolena ingests PDFs, scanned images, emails, and audio and structures their contents into reviewable data.

Reporting, integrations, and downstream actions: Results can be exported as structured reports or pushed into spreadsheets, CRMs, dashboards, and core systems, or used to trigger the next workflow step.

Audit trails and governance controls: The platform records reasoning logs and audit trails and is built around enterprise security, encryption, and governance architecture.

Limitations (based on publicly available sources):

Custom pricing only: Kolena does not publish standard pricing; organizations must contact the vendor for a quote.

Focused on the document layer: Kolena concentrates on document-heavy workflows rather than broad transaction monitoring or regulatory reporting.

Initial setup of agents and integrations: Connecting document sources and configuring agents to match workflows requires initial setup.

Source: Kolena

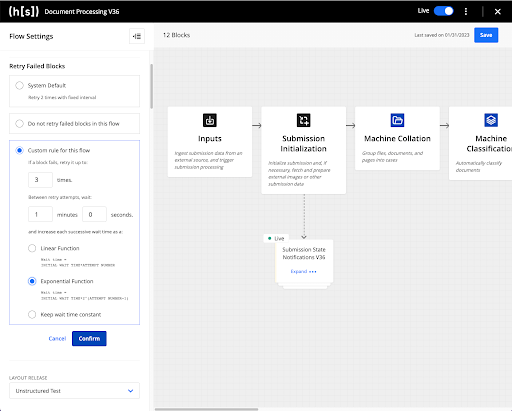

2. Hyperscience

Hyperscience is an intelligent document processing (IDP) platform, currently branded Hypercell, that uses machine-learning models to classify and extract data from a range of documents, including structured forms, semi-structured documents, and unstructured text with handwriting. It is aimed at large enterprises and government agencies, and banks use it to process the documentation that flows through onboarding, lending, and account servicing.

Key features include:

Machine-learning classification and extraction: Hyperscience reads and classifies high volumes of document types and extracts data from structured, semi-structured, and unstructured documents.

Handwriting and complex-document support: The platform handles printed and handwritten text and can extract from longer, more complex documents such as contracts, lease agreements, and loan files.

Human-in-the-loop exception handling: When the system is not confident enough to meet a customer-defined accuracy threshold, it routes the case to a person for review.

Data validation and enrichment: Hyperscience validates and enriches extracted data before it moves downstream, so the information later steps act on is checked first.

Flexible workflow blocks and integrations: The platform provides configurable blocks that can be arranged into flows mapped to a business process, and it integrates with downstream systems.

Security and compliance posture: Hyperscience states it is FedRAMP High authorized and emphasizes security, compliance, and governance for enterprise-scale deployments.

Limitations (as reported by users on G2):

High cost: Reviewers describe the platform as expensive relative to comparable IDP tools, noting that less costly alternatives exist even if they are less capable.

Reliance on model training: Some users report that accuracy and automation are strongest for structured documents and after an upfront training effort, so value depends on investing time in tuning models.

Gaps versus newer AI features: At least one reviewer felt that certain newer AI capabilities trail competing IDP tools.

Smaller user community: Reviewers note a smaller user base than some alternatives, which can mean fewer community resources when looking for help.

Source: Hyperscience

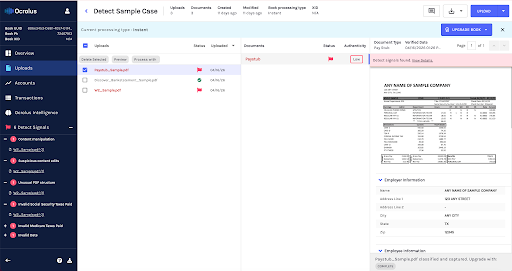

3. Ocrolus

Ocrolus is an AI-powered document automation and analytics platform for lenders and financial services. It specializes in analyzing financial documents such as bank statements, pay stubs, and tax forms with high accuracy, and turning them into data that supports underwriting and credit decisions. The platform combines automated extraction with a human-in-the-loop layer for verification and adds fraud-detection signals on top of the captured data.

Key features include:

Financial document understanding: Ocrolus specializes in capturing data from bank statements, pay stubs, and tax documents with stated accuracy above 99%.

Fraud detection and document integrity: The platform identifies fake documents, data inconsistencies, and risk signals, flagging potential tampering in submitted financial documents.

Cash flow and income analytics: Ocrolus turns captured document data into cash-flow analysis and income calculations, measuring revenue and debt capacity and evaluating income across borrower types.

Human-in-the-loop verification: Ocrolus pairs automated processing with human review as an additional assurance layer, which the vendor describes as combining machine speed with human accuracy.

API and loan-origination integration: The platform is accessible via API and dashboard and integrates into loan origination systems, delivering output directly into existing customer workflows.

Vertical solutions and use cases: Ocrolus offers industry-specific configurations for small-business funding and mortgage, plus use cases spanning consumer lending, auto finance, tax, and tenant screening.

Limitations (as reported by users on Capterra):

Processing speed on complex files: Users report that turnaround can slow for more complicated bank statements, with some processing taking noticeably longer and affecting productivity.

Occasional missed data: Some reviewers note the system can miss information on certain documents, requiring manual double-checking of results.

Communication on product changes: A reviewer described a lack of proactive communication when new analytics and the accompanying guidance were released, requiring them to request updates.

Source: Ocrolus

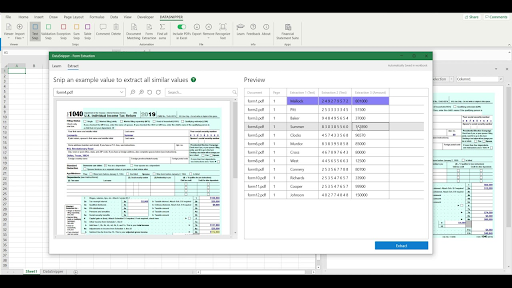

4. DataSnipper

DataSnipper is an automation platform for audit and finance teams that runs inside Microsoft Excel. It is used to collect, extract, cross-reference, and verify data from source documents, automating the documentation and testing work that auditors and financial-control teams perform. For banking, it supports controls testing, financial-statement procedures, and audit preparation, with every extracted value linked back to its source document to create a reviewable evidence chain.

Key features include:

In-Excel extraction and data capture: DataSnipper works inside Excel to extract structured and unstructured data from source documents, turning hours of manual work into review-ready data.

Cross-referencing and reconciliation: The Match capability links Excel data to source documents with full traceability, automating reconciliation such as tying a list in Excel to supporting PDFs.

Document and evidence management: Collecting documents in DataSnipper centralizes financial evidence into one workspace, supporting consistent and compliant collaboration on workpapers.

AI agents for testing and disclosures: Excel Agents automate testing steps inside Excel while keeping the user in control, and Disclosure Agents turn disclosure-checklist reviews into agentic workflows that check statements against standards such as IFRS and GAAP.

Controls and audit support: The platform supports tests of detail, tests of control, walkthroughs, and financial-statement procedures, and lets teams document control testing and supporting evidence directly in Excel.

Standardization across teams: DataSnipper lets organizations standardize procedures across people, teams, and functions, which improves the consistency and quality of documented work.

Limitations (as reported by users on G2):

Performance with large files: Users report slow loading and occasional freezing when handling large financial statements, scanned documents, or large Excel files.

Inconsistent document recognition: Reviewers note that recognition can be inconsistent across varying formats or complex field definitions, sometimes struggling to capture certain text or numbers.

Excel dependency and limited customization: Because it is built around Excel, compatibility with other tools is limited, and some users find customization options and the range of parseable formats constrained.

Source: DataSnipper

Financial Crime Detection and AML Monitoring

These platforms focus on detecting money laundering and other financial crime, monitoring transactions, screening customers against sanctions and watchlists, and managing investigations and regulatory reporting.

5. NICE Actimize

NICE Actimize is a financial-crime, risk, and compliance vendor whose anti-money-laundering platform is widely used by large banks and financial institutions. Its AML suite takes an entity-centric approach, putting the customer entity at the center of risk processes and combining machine learning with domain expertise to detect money laundering and terrorist financing.

Key features include:

Suspicious Activity Monitoring (SAM): SAM provides AML-tuned analytics to cover money-laundering red flags, using behavioral analytics and entity resolution to detect anomalies.

KYC, CDD, and sanctions screening: The suite includes KYC and customer due diligence with event-based triggers to simplify customer risk assessments and reviews, plus sanctions and party screening with advanced matching for real-time payments.

Suspicious Transaction Activity Reporting (STAR): STAR automates the filing of suspicious activity reports to financial intelligence units, auto-populating required fields and using generative AI to draft the report narrative.

Currency Transaction Reporting (CTR): The platform automates CTR filing to help institutions stay compliant with reporting thresholds and requirements.

Enterprise case management (ActOne): ActOne unifies financial-crime, risk, and compliance oversight and reporting into a single case-management environment, giving investigators a consolidated view of risk.

Integrated FRAML and AI tuning: The Xceed offering integrates fraud and AML detection with AI-powered detection, alert triage, and auto-tuning, and supports self-configurable rules.

Limitations (as reported by users on Gartner Peer Insights):

Cost: Reviewers describe the platform as expensive relative to other leading vendors in the market.

Module-based licensing: Because licensing is structured around individual modules, assembling a complete solution can require purchasing several products, which adds to cost.

Support and functionality gaps: Some users report that certain functions did not work as designed and that support responses to tickets were sometimes slow or unsatisfactory.

Source: NICE Actimize

6. Feedzai

Feedzai is an AI-native platform for fraud and financial-crime prevention used by large banks, payment providers, and fintechs. Its RiskOps platform unifies fraud, identity, and AML on a single system, building a continuously updated risk profile of each customer from data such as transaction history, devices, and behavior rather than analyzing transactions in isolation. For AML, Feedzai blends rules and machine learning to monitor transactions, prioritize alerts, and reduce false positives, and it integrates sanctions, PEP, and watchlist screening.

Key features include:

AML transaction monitoring: Feedzai uses rules combined with machine learning to identify potential money-laundering and terrorist-financing patterns and to prioritize alerts, letting investigators focus on higher-risk cases.

Watchlist and sanctions screening: The platform integrates sanctions, PEP, and watchlist screening, automating alerts and documenting decisions so institutions can block prohibited transactions and demonstrate compliance.

Unified RiskOps platform: Rather than separate tools for fraud, identity, and AML, Feedzai brings these together in one cloud-based system that synthesizes data across the customer lifecycle.

Behavioral, entity-level profiling: Feedzai builds a profile of each customer using transactional, behavioral, device, and network data to detect anomalies against that baseline.

Integrated SAR filing: The platform auto-populates fields for suspicious activity report submission, reducing manual input and simplifying the regulatory filing process.

Explainable AI and scalability: Feedzai includes responsible-AI tooling that explains why a decision was made and supports self-service model and rule changes, plus real-time scoring at large scale.

Limitations (based on publicly available sources):

Complexity for non-specialists: Reviewers note that the platform's power comes with complexity and that it is not well suited to users with little experience administering fraud and financial-crime products.

Cost: Users describe the platform as carrying a fairly high cost, though some add that it is in line with comparable competitors.

Support depth on complex cases: Some reviewers see room for improvement in support responsiveness and depth during more complex or time-sensitive situations.

Cloud-versus-on-premise gap: Newer and more advanced capabilities are noted as being available in the cloud version, with older on-premise deployments lagging behind.

Source: Feedzai

7. ComplyAdvantage

ComplyAdvantage is an AML and financial-crime risk platform whose product, ComplyAdvantage Mesh, is a cloud-based system that combines the company's proprietary risk-intelligence database with AML applications. It is used by banks, payment firms, and fintechs to screen customers and monitor behavior in near real time across the customer lifecycle.

Key features include:

Customer, company, and payment screening: Mesh screens individuals and companies against sanctions, watchlists, PEPs, and adverse media, and screens payments, supporting both onboarding and ongoing checks.

Transaction and ongoing monitoring: The platform monitors transactions and customer behavior in near real time, surfacing evolving risks and prioritizing alerts by risk level and type.

Risk scoring: Mesh produces automated, configurable risk scores across customers and events, dynamically updated as new information arrives. This gives a data-driven view of each person or company's risk.

Case management: Alert reviews and investigations are managed within the platform, with collaboration across teams and a full audit trail capturing when and why decisions were made.

Agentic auto-remediation: Mesh uses agentic AI to review and complete compliance workflows end to end, processing approximately 65 to 85 percent of profiles automatically.

Security and integration: The platform is SOC 2 Type II and ISO 27001 certified, with encryption in transit and at rest and role-based permissions, and it offers real-time API, batch, and SFTP integration options.

Limitations (as reported by users on G2):

False positives: Reviewers report that screening can produce false positives that require additional manual review, adding to workload.

User interface: Some users describe the interface as clunky and note workflow friction, such as a notes field that does not clearly separate different hits.

Customization and integration complexity: A few reviewers find the customization and API integration involved, requiring effort to configure to their needs.

Data accuracy: Some reviews cite occasional data inaccuracies during screening.

Source: ComplyAdvantage

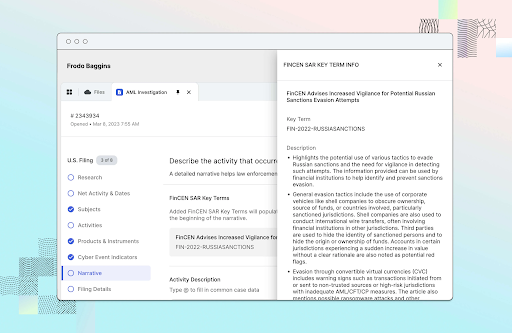

8. Hummingbird

Hummingbird is a risk and compliance platform purpose-built for financial-crime investigations, used by banks, fintechs, and crypto firms. It acts as a single source of truth that brings together customer data, case management, investigations, and regulatory reporting, so cases can be worked from any starting point, whether transaction-monitoring alerts, fraud alerts, or flagged KYC and KYB checks.

Key features include:

Investigations and case management: Hummingbird unifies customer data, case information, and investigative tooling, including data visualizations, customer profiles, and integrated requests for information, so investigators can connect the dots without switching systems.

Automated regulatory reporting: The platform's patented filing technology automates report generation for suspicious activity reports and supports electronic filing to financial intelligence units, including FinCEN, FINTRAC, and goAML countries.

Alert triage and de-duplication: Hummingbird groups and de-duplicates transaction-monitoring alerts and organizes cases automatically, reducing repetitive dispositioning.

No-code process automation and AI: The platform lets teams identify and automate repetitive tasks without code, and its AI tools, including agents and an assistant, can handle more complex tasks.

Customer screening and monitoring: Newer solutions add sanctions, PEP, and adverse-media screening and transaction-and-risk monitoring, with access to third-party data sources through the platform.

Oversight, audit trails, and integrations: Configurable dashboards, reports, and an activity log provide program oversight and keep teams audit-ready, and the platform connects to core systems and third-party data sources.

Limitations (based on publicly available sources):

Investigation focus: The platform is centered on investigation, case management, and reporting; while it has added monitoring and screening, organizations may still need separate systems for full transaction monitoring, sanctions screening, or fraud decisioning.

Integration dependency: Its value depends on connecting to upstream alert sources, data repositories, and reporting systems; where integrations are limited, investigators may need to duplicate data entry, and integration scope can vary by environment.

Configuration governance: Configurable workflows and fields require clear internal governance to avoid inconsistent case handling across teams.

Pricing transparency: Pricing is not published and is provided on request, which can complicate upfront budgeting.

Source: Hummingbird

Governance, Risk, and Regulatory Compliance Platforms

These platforms provide the governance backbone for compliance programs, consolidating risk and compliance data, mapping regulatory requirements to controls and policies, and managing audit, reporting, and client lifecycle obligations across the enterprise.

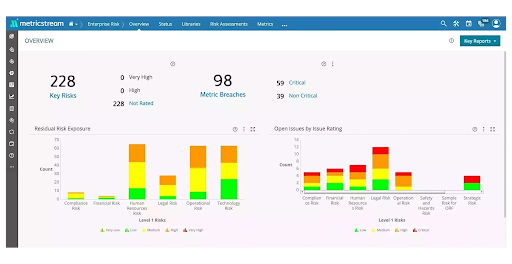

9. MetricStream

MetricStream is a governance, risk, and compliance (GRC) software vendor whose connected GRC platform helps banks and other enterprises manage risk and compliance across previously siloed functions in a single environment. It serves banking and financial services among other sectors and spans enterprise and operational risk, regulatory compliance, regulatory change, internal audit, SOX, IT and cyber risk, third-party risk, policy management, and resilience.

Key features include:

Regulatory compliance and change management: MetricStream helps institutions manage compliance with federal, state, and local regulations, align internal policies to those requirements, and track regulatory changes and assess their impact.

Enterprise and operational risk management: The platform provides a standardized, enterprise-wide risk framework with uniform assessment methodologies and simplified processes for identifying, assessing, monitoring, and mitigating risk.

Internal audit and SOX controls: MetricStream supports risk-based audit planning, scheduling, workpaper management, execution, and follow-up, plus SOX surveys, certification, and control testing.

Third-party risk management: The platform identifies, assesses, mitigates, and monitors third- and fourth-party risks and tracks performance through a single reference point.

Control rationalization across frameworks: A shared library lets a single control satisfy requirements from several regulations, reducing the number of assessments needed.

Embedded AI and reporting: AI classifies issues, identifies duplicate findings, recommends remediation, and monitors key risk indicators, while role-based dashboards translate GRC data into reporting for executives and the board.

Limitations (as reported by users on Gartner Peer Insights):

Implementation complexity: Reviewers describe a steep learning curve and significant configuration and deployment effort, with the structure feeling overwhelming and reworking reports often requiring IT support.

Customization rigidity: Some users find the platform rigid for custom changes, with configuration and deployment taking considerable time.

Support experience: Several reviewers report that resolving issues can take multiple interactions with the support team and that custom integrations with non-standard products are resource-intensive.

Usability and automation gaps: Some note that the user experience is not always intuitive and that an unexpected amount of manual work can remain.

Source: MetricStream

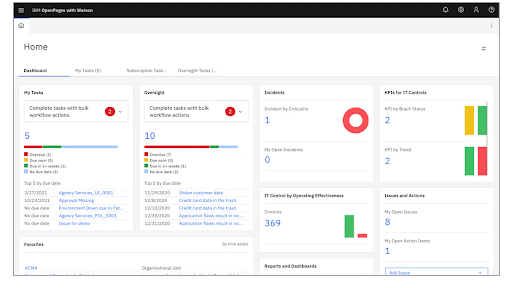

10. IBM OpenPages

IBM OpenPages is an AI-driven governance, risk, and compliance platform that centralizes siloed risk-management functions in one environment to identify, manage, monitor, and report on risk and regulatory compliance. It runs on any cloud or on-premises and takes a modular approach, so banks can deploy only the domains they need, including operational risk, regulatory compliance, financial controls, internal audit, IT governance, model risk, third-party risk, policy, data privacy, and ESG.

Key features include:

Regulatory compliance management module: OpenPages provides a single repository to manage regulatory content and classify large volumes of regulatory data, automating identification of regulatory changes and breaking regulations into a catalog of requirements with assigned owners.

Mapping requirements to risks and controls: The platform maps regulatory requirements to internal risk data, connecting them to key risks, controls, and policies in firm-specific terms.

Modular GRC domains: OpenPages offers domain-targeted modules covering operational risk, financial controls, internal audit, IT governance, model risk, third-party risk, policy, data privacy, business continuity, and ESG.

Embedded and bring-your-own AI: AI automates classification and issue creation and powers recommendations, and an API-based architecture lets organizations connect IBM watsonx.ai or third-party and custom models.

Visualization and enterprise scale: The GRC Canvas is an interactive workspace for modeling processes, risks, and controls with live data, and the configurable, low-code platform scales across all lines of defense to large organizations.

Integrations and reporting: Open integrations connect business-intelligence tools, data platforms, and external systems to export and analyze GRC data, supporting traceability and audit readiness.

Limitations (as reported by users on Gartner Peer Insights):

Interface and usability: Reviewers describe the user interface as not modern or intuitive, with unclear field meanings, extra confirmation clicks for simple tasks, and a learning curve for onboarding end users.

Reporting dependence on external tools: Some users note that data still needs to be exported into Excel and PowerPoint for board reporting, and that report generation can be slow.

Cost: Reviewers describe the platform as expensive relative to other GRC tools.

Deployment effort: Some report that migration and deployment can be difficult and that certain setup actions lack embedded controls.

Source: IBM

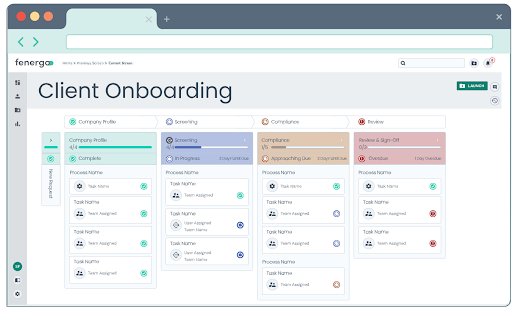

11. Fenergo

Fenergo provides client lifecycle management (CLM) software for financial institutions, digitally managing clients from onboarding and KYC through ongoing reviews and offboarding. It is used by banks, asset managers, and other financial firms to simplify client onboarding while maintaining regulatory compliance across more than 120 jurisdictions. Fenergo's platform orchestrates the client journey, manages client and related-party data in a central repository, and runs a policy and rules engine that determines KYC and AML requirements at each stage.

Key features include:

Client lifecycle management and onboarding: Fenergo orchestrates client journeys from prospecting and digital account opening through maintenance, refresh, ongoing due diligence, and offboarding.

Know Your Customer across jurisdictions: The KYC solution applies enterprise-wide standards across more than 120 jurisdictions, using a policy engine to determine KYC and AML requirements at each stage and supporting identification of beneficial owners and complex ownership hierarchies.

Regulatory rules engine: Fenergo's rules engine supports compliance obligations across many regulations, including AML and counter-terrorist financing, tax frameworks such as FATCA, AEOI, and CRS, ESG, OTC derivative reforms, data privacy, and investor protection.

Client and related-party data management: The platform digitally captures and re-uses client and related-party data in a central repository, providing a single client view that can be re-used across the enterprise for regulatory and business purposes.

Risk assessment engine: Fenergo automates on-demand financial-crime risk assessment of clients and related parties, providing a centralized source for managing multiple, complex risk models.

Transaction monitoring and AI agents: The platform includes transaction monitoring and a set of AI agents, including ones for document classification and extraction, KYC data sourcing, and flagging significant client-data changes, that automate parts of onboarding and review.

Limitations (based on publicly available sources):

Implementation effort: As an enterprise CLM platform with a deep rules engine spanning many jurisdictions, deployments typically require significant time, technical resources, and integration work.

Workflow friction on edits: A user noted that revising previously completed fields can require repeating steps, adding friction within in-flight cases.

Enterprise orientation and pricing: The platform is geared to mid-to-large financial institutions and is priced at the enterprise level with custom quotes, which can place it out of reach for smaller teams.

Integration dependency: Realizing full value depends on integrating data providers and core systems via APIs, so onboarding and data-integration effort is non-trivial.

Source: Fenergo

Conclusion

Banking compliance automation helps financial institutions manage growing regulatory requirements while improving operational efficiency, accuracy, and audit readiness. By automating document reviews, due diligence workflows, compliance monitoring, and reporting activities, banks can reduce manual effort, strengthen risk management, and respond more quickly to regulatory changes. As compliance obligations continue to evolve, automation provides a scalable foundation for maintaining control, reducing operational risk, and supporting a more proactive compliance program.