What Is FNMA Form 1004 (Uniform Residential Appraisal Report)?

Fannie Mae Form 1004, also known as the Uniform Residential Appraisal Report (URAR), is the industry-standard document used by appraisers to determine the market value of a single-family residential property. Lenders rely on this comprehensive assessment to approve mortgage loans:

Key details and characteristics

Property types: Used primarily for detached single-family homes, properties in Planned Unit Developments (PUDs), and one-unit properties with accessory dwelling units.

Variations: Alongside the traditional on-site inspection form, Fannie Mae also offers Form 1004 Desktop (no interior inspection) and Form 1004 Hybrid (third-party data collection) to accommodate modern valuation methods.

Methodologies: The form guides the appraiser through three primary valuation approaches: the cost approach, sales comparison approach, and income approach.

Exclusions: It is not intended for manufactured homes, co-ops, or condominium units.

Standard sections:

A completed Form 1004 typically features the following:

Subject and contract: Basic property details, legal description, assessor's parcel number, and sales contract data.

Neighborhood analysis: Market trends, property values, and demand/supply conditions in the immediate area.

Site and improvements: Lot size, zoning compliance, utility access, FEMA flood zones, and physical condition.

Cost approach: An estimation of the cost to rebuild the property from scratch minus depreciation.

Sales comparison approach: A detailed comparison matrix analyzing recent, nearby sales of similar homes.

This is part of a series of articles about FNMA Forms.

When Is FNMA Form 1004 Used?

Conventional Mortgage Loans

FNMA Form 1004 is most commonly used for conventional mortgage loans, which are home loans not insured or guaranteed by government agencies such as the FHA, VA, or USDA. Lenders selling loans to Fannie Mae or Freddie Mac require a standardized assessment of the collateral’s value, making the 1004 form their preferred choice for single-family properties. The form’s analysis helps lenders verify that the property meets underwriting guidelines and supports the loan amount requested by the borrower.

The use of the 1004 form in conventional loans ensures that lenders, investors, and regulators can trust the consistency of the property valuation. By adhering to Fannie Mae standards, appraisers help reduce risk in the lending process and enable loans to be packaged and sold on the secondary mortgage market. This widespread use makes FNMA Form 1004 a central component in the conventional mortgage industry.

One-Unit Residential Properties

FNMA Form 1004 is designed for the appraisal of one-unit residential properties, including detached single-family homes, townhouses, and certain types of planned unit developments (PUDs). The form is not intended for multi-unit dwellings, condominiums, or manufactured homes, each of which has its own designated appraisal form. Appraisers use the 1004 form to document the condition, features, and market position of the property being evaluated, ensuring that the property meets Fannie Mae eligibility requirements for a conventional mortgage.

The focus on one-unit residential properties allows the 1004 form to address the characteristics and market factors affecting this segment of real estate. By limiting its use to these property types, the form avoids the complexities associated with multifamily or specialized housing and simplifies the appraisal process for most conventional home loans.

Related content: Discover the top use cases for AI in real estate.

When Another Appraisal Form May Be Required

There are instances where FNMA Form 1004 is not appropriate and another appraisal form is required. For example, properties with more than one unit, such as duplexes or triplexes, require Form 1025 (Small Residential Income Property Appraisal Report). Condominiums are appraised using Form 1073, which is tailored to condo ownership and market characteristics. Manufactured homes use Form 1004C to address specific construction and valuation factors.

Selecting the correct appraisal form is critical for lenders and appraisers to comply with Fannie Mae guidelines. Using the wrong form can lead to underwriting issues, delays, or loan denial. Appraisers must assess the property type at the outset of the assignment to ensure the correct reporting format is used.

Key Details and Characteristics of FNMA Form 1004 [QG1]

Property Types

FNMA Form 1004 is limited to one-unit residential properties that are not condos or manufactured homes. This includes single-family detached houses, attached townhouses, and some planned unit developments (PUDs) with individual ownership. The form is not suitable for commercial properties or multi-unit buildings, which require additional analysis. By focusing on a narrow property type, the form supports a standardized approach to residential appraisals and helps underwriters interpret findings.

The property type determines the form used, the scope of the appraisal, and the level of detail required. For example, appraisals for homes in planned unit developments may require analysis of HOA fees and common area amenities. The 1004 form includes sections for these details.

Variations

There are several variations of the FNMA 1004 form for different appraisal scenarios:

The most common is the standard 1004, used for full interior and exterior inspections.

The 1004C is designated for manufactured homes.

The 1004D serves as an update or completion report for previously appraised properties.

Another variation is the 1004 Desktop, which allows appraisers to complete the report without a physical inspection, using third-party data and digital resources.

Each variation aligns with specific Fannie Mae guidelines and property characteristics. Lenders select the appropriate version based on the property type, loan purpose, and risk tolerance. These variations allow flexibility while maintaining the standardized reporting structure required by Fannie Mae and the secondary mortgage market.

Methodologies

FNMA Form 1004 requires appraisers to use multiple valuation methodologies, primarily the sales comparison and cost approaches:

The sales comparison approach is typically the most heavily weighted, requiring analysis of at least three recent sales of comparable properties in the neighborhood. Adjustments are made for differences in features, condition, and location to reach a value estimate.

The cost approach is included to provide an alternative perspective based on land value and replacement cost.

Using multiple methodologies strengthens the appraisal by providing checks on the value estimate. Each approach has strengths and limitations, but together they help ensure the final valuation reflects market conditions and property-specific factors.

Exclusions

FNMA Form 1004 is not suitable for every property type or lending scenario. Properties with commercial use, agricultural land, or significant income from multiple units are excluded. Fannie Mae requires specialized appraisal forms for these cases. Using the 1004 form for ineligible properties can result in loan rejection or compliance issues during review.

The 1004 form is also not intended for properties with atypical zoning, complex ownership structures, or that fall outside the standard definition of a one-unit residence. Appraisers and lenders must review Fannie Mae eligibility requirements before assigning the 1004 form.

Understanding FNMA Form 1004

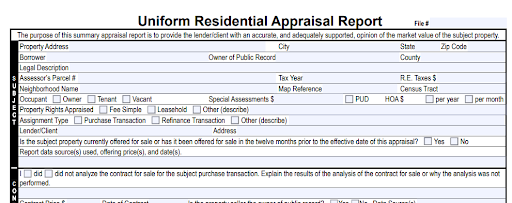

1. Subject and Contract

The “Subject” section of FNMA Form 1004 captures information about the property being appraised, including address, legal description, and owner’s name. This section also records the intended use and user of the appraisal. Appraisers verify the property’s legal and physical characteristics, including parcel number and location.

The “Contract” section provides details about the pending sale, if applicable, including contract price, date, and any terms that may affect value. Appraisers analyze the contract to identify concessions, incentives, or unusual conditions that could influence market value.

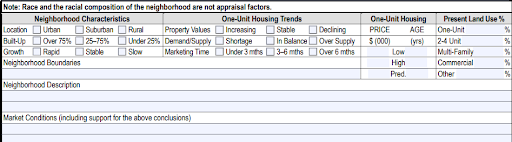

2. Neighborhood Analysis

The neighborhood analysis section requires the appraiser to examine the market context in which the subject property exists. Factors such as location, market trends, economic influences, and neighborhood characteristics are documented. The appraiser assesses property values, market stability, demand and supply balance, and external factors that could affect desirability or risk.

This analysis helps determine how the subject property compares to others in the area and identify potential risks. Trends in property values, changes in land use, or shifts in population demographics can affect the appraised value.

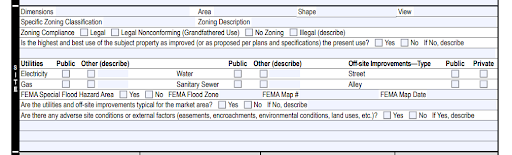

3. Site and Improvements

The “Site” section documents the physical characteristics of the land on which the property is located. Appraisers record details such as lot size, zoning classification, utility availability, flood zone status, and adverse site conditions. These factors can influence marketability and value, especially when the site has limitations related to access, topography, or legal restrictions.

The “Improvements” section focuses on the dwelling and other structures on the property. Appraisers evaluate the home’s age, design, construction quality, condition, room count, gross living area, and recent updates or renovations. They also identify deferred maintenance or physical deficiencies that may affect value.

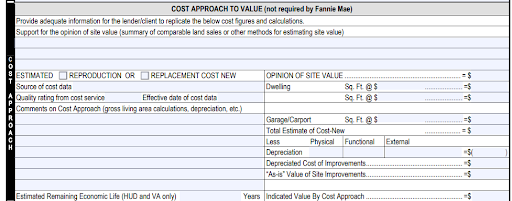

4. Cost Approach

The cost approach estimates value by calculating the cost to replace or reproduce the improvements, adjusting for depreciation, and adding land value. Appraisers rely on recognized cost services and local market data to estimate replacement costs. Depreciation may include physical wear and tear, functional obsolescence, or external influences.

While the cost approach is often given less weight than the sales comparison approach for existing homes, it remains part of FNMA Form 1004. It can be useful for newer homes or in markets with limited comparable sales.

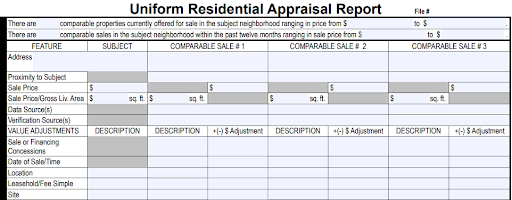

5. Sales Comparison Approach

The sales comparison approach is generally the primary valuation method used in FNMA Form 1004. Appraisers select recent sales of similar properties, referred to as comparables or “comps,” and compare them to the subject property. Adjustments are made for differences in size, condition, age, location, lot size, amenities, and upgrades.

The form includes a standardized grid that allows underwriters and reviewers to evaluate comparable sales and adjustments. Appraisers must explain significant adjustments and justify the relevance of each comparable. By analyzing market transactions, the sales comparison approach provides the main support for the final opinion of market value.

Related articles: FNMA 1007 Form and FNMA 1003 Form.

FNMA Form 1004 vs. 1004 Desktop

FNMA Form 1004 Desktop is a modified version of the standard 1004 appraisal report. The main difference is the inspection process. A standard 1004 requires the appraiser to complete an interior and exterior inspection. A 1004 Desktop allows the appraiser to complete the appraisal without visiting the property:

With a 1004 Desktop, the appraiser relies on data sources such as public records, multiple listing service data, property photos, floor plans, prior appraisals, and third-party inspections. The appraiser must still develop an independent opinion of value and determine whether the available information supports the assignment.

The standard 1004 is generally used when a full inspection is required or when the property has condition concerns, unusual features, or limited data. The desktop version is used in eligible lending scenarios where Fannie Mae guidelines allow a reduced inspection scope.

Both forms estimate the market value of a one-unit residential property for mortgage lending. Form 1004 is inspection-based, while Form 1004 Desktop is data-based. The choice depends on loan eligibility, risk level, investor requirements, and whether sufficient property information is available without an on-site inspection.

How AI Can Help Review FNMA Form 1004 More Efficiently

AI can be useful for reviewing forms like Uniform Residential Appraisal Report:

AI can speed up FNMA Form 1004 review: It does this by extracting key data from appraisal documents, supporting files, spreadsheets, scans, and emails. This can include property details, comparable sales, condition ratings, adjustments, and valuation conclusions.

It can apply business rules and cross-checks to validate the report: For example, AI can compare values across sections, flag missing fields, identify unusual adjustments, and surface inconsistencies between the appraisal, loan file, and supporting documents.

It can improve transparency: Each extracted value or flagged issue can include citations, reasoning, and confidence scores, helping reviewers verify the result instead of relying on a black-box output.

AI can generate structured outputs for downstream workflows: Appraisal review findings can be exported to spreadsheets, reporting tools, CRMs, document systems, or internal approval workflows. This reduces manual data entry and helps teams process higher volumes without changing their existing systems.

Related content: Learn how AI-powered underwriting software speeds up real estate and lending decisions.

How to Review FNMA Form 1004 Faster with Kolena

Reviewing a Uniform Residential Appraisal Report manually means working line by line through subject data, neighborhood analysis, cost and sales comparison grids, and adjustments — a slow, error-prone process. Kolena's free AI Appraisal Report Abstraction tool lets you upload a 1004, 1025, or other appraisal report and analyze it with AI, returning an instant, AI-generated abstract that extracts the key information in seconds — securely, accurately, and at no cost.

Key capabilities of Kolena's AI Appraisal Report Abstraction tool:

Instant appraisal abstraction: Upload 1004, 1025, or other appraisal reports and receive an AI-generated abstract in seconds, with key data extracted automatically.

Secure, private processing: The tool is SOC 2 compliant and does not train AI on your data.

No signup to get started: Run appraisal reports through the tool for free, with no signup required.

Customizable AI agent: Clone the agent into your own account and tailor it to your exact specifications, workflows, policies, templates, and documents.

Built to run at scale: Move beyond one-off reviews to analyze appraisal reports at scale across your document workflows.

Ready to speed up your appraisal reviews? Try Kolena's free AI Appraisal Report Abstraction tool and turn a full 1004 into a structured abstract in seconds.