What Are ACORD Forms?

ACORD Forms are standardized insurance documents developed by ACORD Solutions Group (Association for Cooperative Operations Research and Development) to streamline data exchange in the insurance industry, creating consistent formats for applications, certificates (like the famous ACORD 25), loss notices, and policy changes.

These digital and printable forms ensure everyone uses the same language, reducing errors and speeding up processes like quoting and binding coverage. In essence, ACORD forms are the universal language of the insurance business, ensuring everyone from a small business owner to a large carrier understands the essential policy details.

Here are the main types of ACORD Forms:

ACORD 25: Provides proof of liability insurance to third parties for contractual or business requirements.

ACORD 125: Core commercial application form capturing general business and policy request details.

ACORD 126: Adds detailed information about general liability exposures and coverage selections.

ACORD 140: Documents commercial property risks, values, and protection details for underwriting.

ACORD 130: Collects payroll, employee data, and loss history for workers compensation coverage.

ACORD 131: Specifies excess or umbrella coverage needs and schedules underlying policies.

ACORD 127: Lists business autos, drivers, and vehicle use details for commercial auto policies.

ACORD 146: Covers mobile equipment like tools or machinery not insured under standard property forms.

We describe each of these forms in more detail below.

In this article:

Key Functions of ACORD Forms

Standardized Information Exchange

ACORD forms function as a common language for the insurance industry, ensuring accurate transfer of key data between different stakeholders. By having a prescribed layout, structure, and data format, these forms reduce the potential for ambiguity or misinterpretation. This benefit extends beyond policyholders and agents to insurers, reinsurers, and regulators.

The consistency that ACORD forms provide accelerates transactions and minimizes the need for redundant data entry. Information exchanged via ACORD forms can feed directly into management, rating, or claims systems, reducing labor and transcription errors.

Policy Application and Underwriting Support

ACORD forms are pivotal during policy applications by gathering detailed, standardized data for underwriting risk assessment. Through specific forms, such as ACORD 125 for commercial lines or ACORD 130 for workers’ compensation, insurance professionals collect the relevant exposures, locations, operations, and loss history that underwriters require to accurately price coverage.

During the underwriting review, these completed forms support the consistent evaluation of risk across multiple submissions and carriers, enhancing comparison and decision-making. The structured design ensures underwriters receive all needed information up front, reducing unnecessary follow-ups and delays.

Policy Servicing and Endorsements

Managing active insurance policies often involves changes, updates, and endorsements. ACORD forms provide a standard approach to submitting these changes, whether an insured party adds coverage, updates addresses, or revises limits. For example, forms like ACORD 126 (general liability) and ACORD 140 (property) handle requests for policy modifications.

By relying on standardized ACORD endorsement forms, agencies and carriers can process change requests efficiently and ensure accurate documentation. This reduces the risk of administrative errors, missed coverage changes, and compliance problems.

Claims Reporting and Processing

ACORD provides forms like the ACORD 1 and ACORD 2 for reporting property and automobile losses, respectively. These forms prompt agents or insured parties to supply all critical claim information—including policy details, event descriptions, and loss data—using defined fields. This speeds up initial claims intake and aligns all parties on the facts as the claim progresses.

Standardized claims forms streamline processing by feeding data directly into carrier claims management systems, triggering automated workflows and documentation trails. This structure reduces manual handoffs, accelerates payment or denial decisions, and allows audit-friendly recordkeeping.

Regulatory and Compliance Documentation

Insurance carriers, agencies, and insureds face ongoing regulatory requirements for transparency, data retention, and consumer protection. ACORD forms play a crucial role in meeting these obligations by offering pre-approved templates that comply with state and federal legal mandates. Common examples include Evidence of Property Insurance (ACORD 28) and Certificates of Insurance (ACORD 25), which are required in many business transactions.

Using ACORD forms as compliance documentation ensures that all stakeholders use the latest, regulator-approved language and disclosures. This decreases the risk of regulatory scrutiny or market conduct criticism. In events like audits or disputes, having properly executed ACORD forms can serve as definitive proof of coverage, application, and customer notification.

Benefits of Using ACORD Forms

ACORD forms provide measurable operational and strategic advantages for insurance professionals. Their consistent structure, broad industry acceptance, and integration with core systems make them a key enabler of efficiency and accuracy across the insurance value chain.

Key benefits include:

Operational efficiency: ACORD forms reduce the need for duplicate data entry and minimize manual handling. Standardized layouts allow automation tools to extract and validate information quickly, cutting down processing time and administrative overhead.

Data accuracy and consistency: Using defined fields and formats minimizes interpretation errors and ensures consistency across documents. This improves data quality and reduces back-and-forth between stakeholders to clarify submissions.

System integration: ACORD forms are designed to integrate with agency management systems, underwriting platforms, and claims systems. This compatibility supports faster data flow, fewer transcription errors, and more reliable system-to-system communication.

Regulatory compliance: Since ACORD maintains its forms in alignment with regulatory requirements, using them helps carriers and agents meet state and federal documentation standards with less legal risk.

Interoperability across markets: The wide acceptance of ACORD forms ensures that documentation is recognized and processed efficiently across different carriers, brokers, and regions. This standardization supports smoother collaboration in both domestic and international markets.

Faster client service: With a reduced need for manual review and clarification, agencies can respond more quickly to client needs—from quoting and binding to issuing certificates or processing claims.

Key Types of ACORD Forms

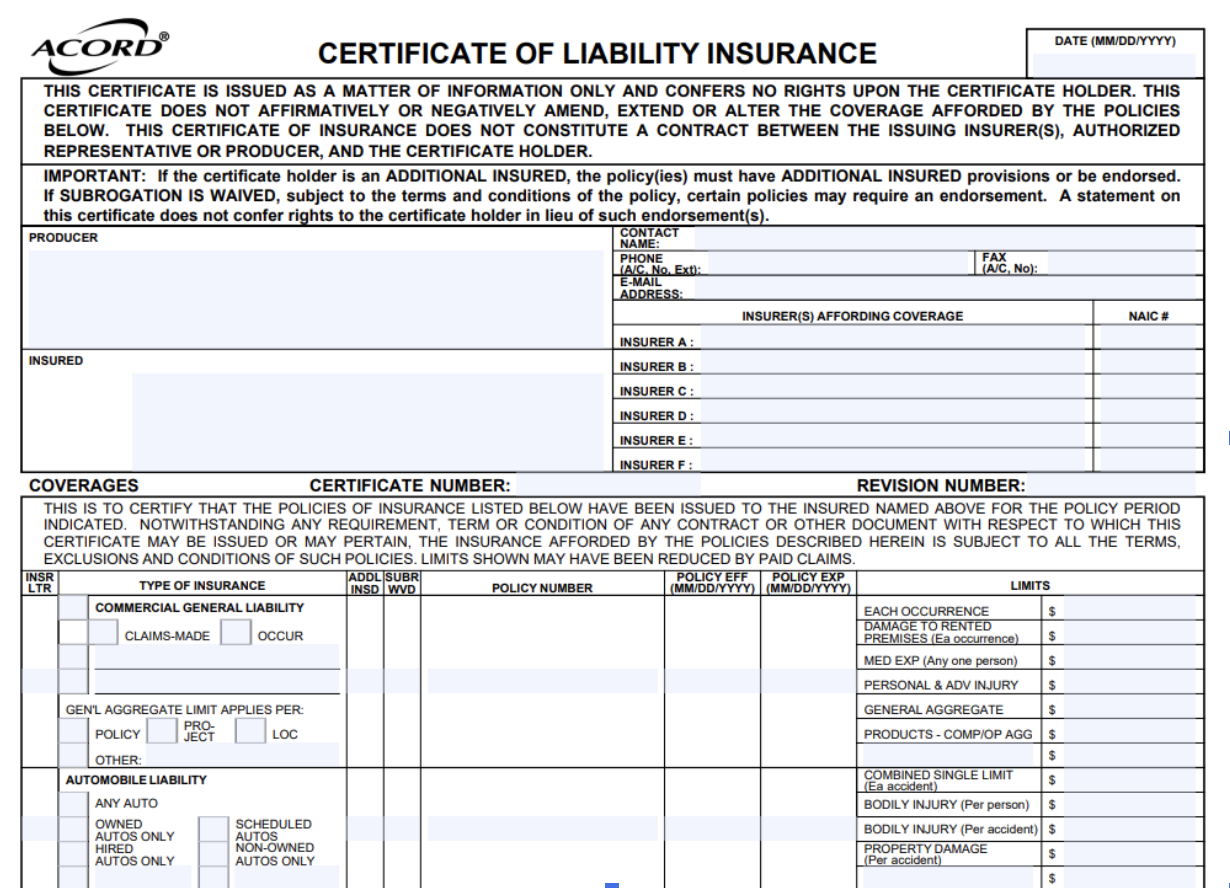

ACORD 25

The ACORD 25, Certificate of Liability Insurance, is the standard document used to provide evidence of liability coverage to third parties. It summarizes core policy details, including insurer name, policy numbers, coverage types, limits, and effective and expiration dates. Landlords, project owners, lenders, and counterparties commonly require this form before allowing work to begin or contracts to take effect.

The ACORD 25 does not modify coverage and is not an insurance contract. It reflects information as of the date issued and explicitly states that it confers no rights on the certificate holder. Any change to coverage must be made by endorsement to the underlying policy, not by altering the certificate.

Guidelines for filling the form:

Enter the named insured exactly as it appears on the policy declarations.

List each coverage line with the correct policy number, limits, and policy period.

Verify that limits meet contractual requirements before issuing the certificate.

Include additional insured information only if supported by an endorsement.

Avoid adding non-standard language or modifying preprinted wording.

Confirm the certificate holder name and address match the contract.

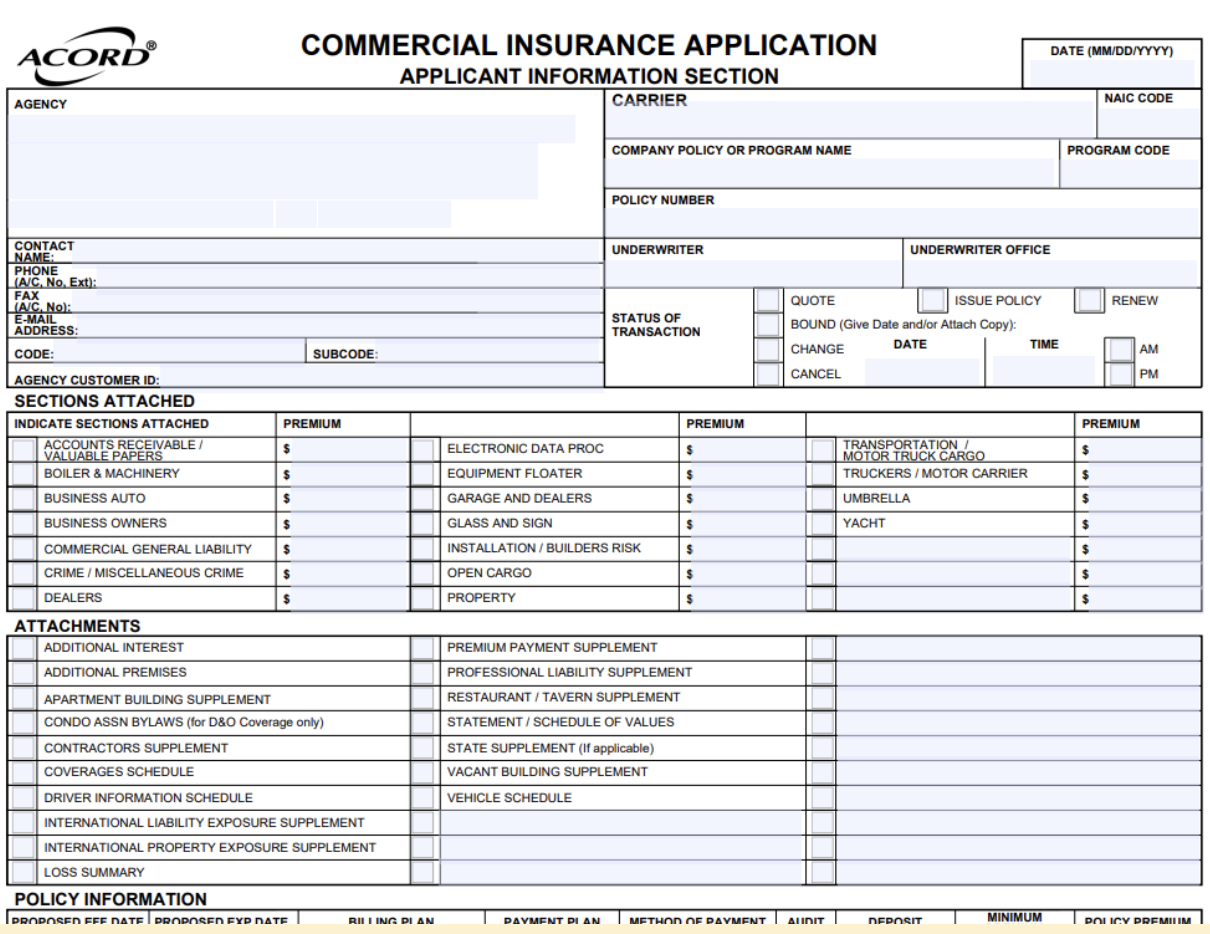

ACORD 125

The ACORD 125, Commercial Insurance Application, serves as the primary intake form for commercial property and casualty submissions. It captures applicant information, business operations, contact details, prior coverage, and loss history. This form establishes the baseline profile of the risk and is typically submitted together with line-specific forms.

Underwriters use ACORD 125 to understand the nature of the business, years in operation, ownership structure, and requested lines of insurance. Its standardized layout enables agencies to submit consistent data across multiple carriers and supports automated intake within underwriting systems.

Guidelines for filling the form:

Provide complete legal entity information, including FEIN and years in business.

Describe operations clearly and consistently with classification codes.

Disclose prior carrier information and at least three to five years of loss history.

Indicate all requested lines of business and attach supporting ACORD sections.

Ensure signatures and dates are included where required.

Review for internal consistency across all attached forms.

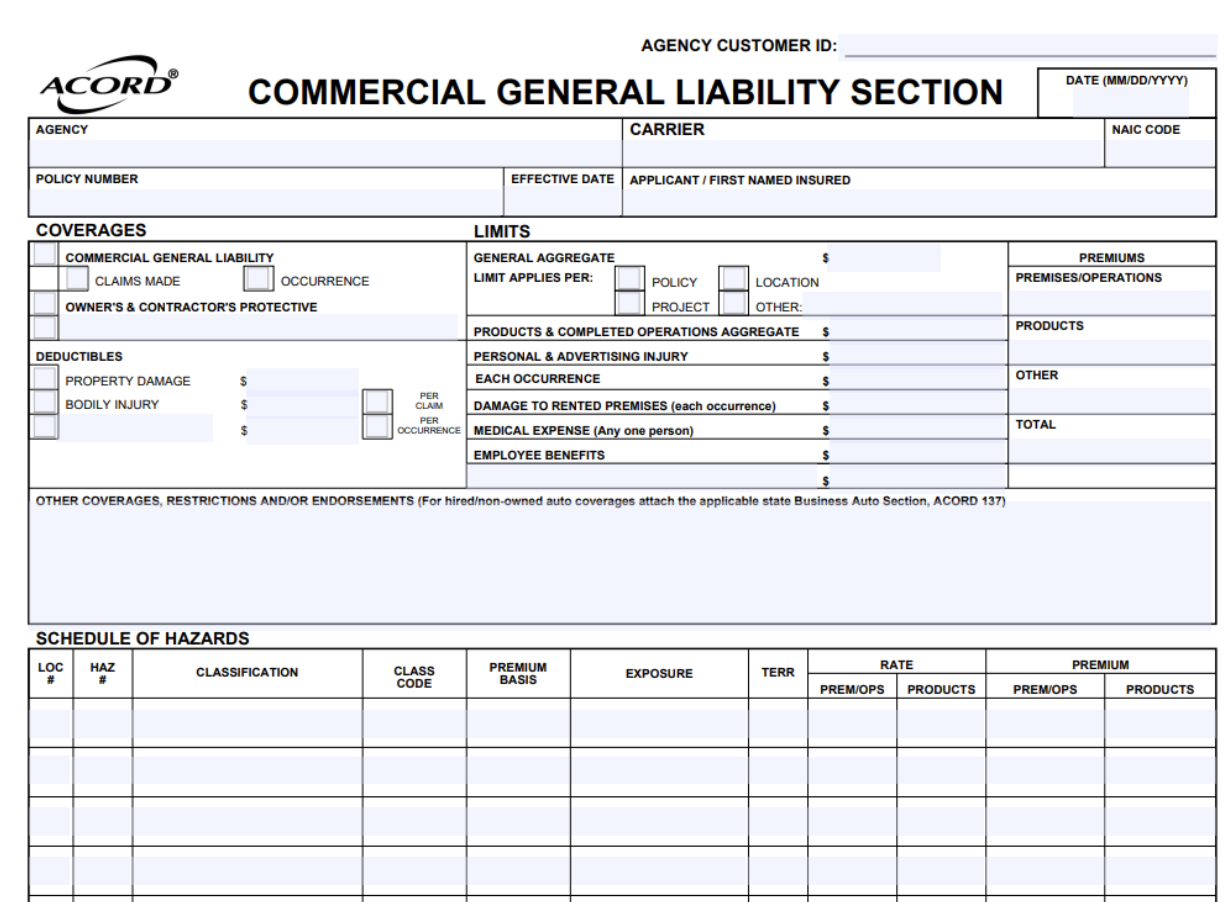

ACORD 126

The ACORD 126, Commercial General Liability Section, supplements ACORD 125 when liability coverage is requested. It gathers detailed data about premises, operations, products, completed operations, subcontractors, and risk controls. The form supports underwriting evaluation of exposure to bodily injury and property damage claims.

Information provided in ACORD 126 influences classification, rating, exclusions, and endorsement requirements. Accurate disclosure of operations and contractual exposures reduces the likelihood of coverage disputes or post-bind corrections.

Guidelines for filling the form:

Provide a detailed description of operations, including subcontracted work.

Identify all premises and confirm square footage and occupancy details.

Disclose prior liability claims and explain any large or unusual losses.

Indicate requested limits, deductibles, and occurrence or claims-made basis.

Note any additional insured or waiver of subrogation requirements.

Confirm responses align with representations made in the main application.

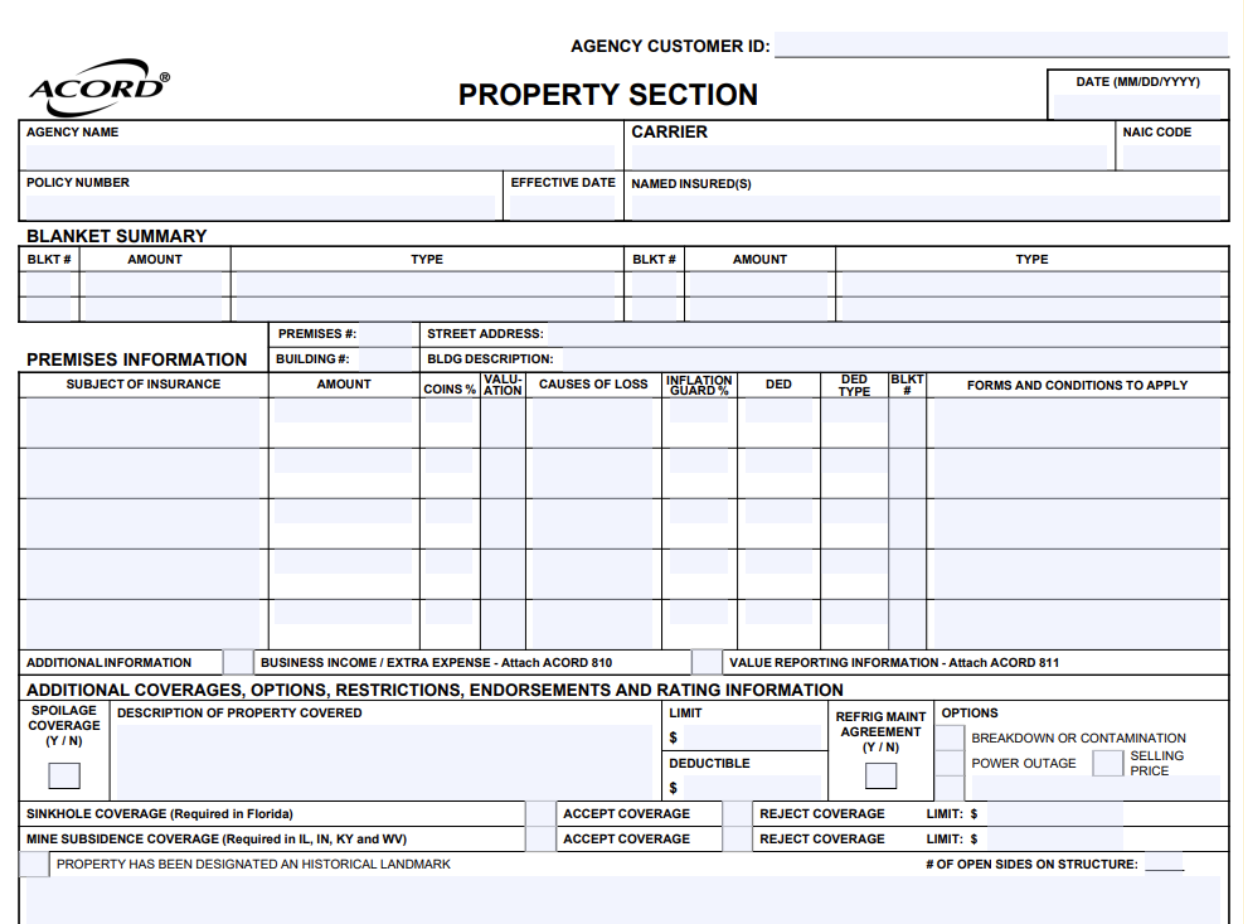

ACORD 140

The ACORD 140, Property Section, captures exposure data for commercial property risks. It includes location schedules, construction type, occupancy, protection class, valuation method, and coverage amounts. Underwriters rely on this data to evaluate susceptibility to fire, theft, wind, and other property perils.

Each insured location must be clearly documented, including building and contents values. The form supports accurate rating and helps determine appropriate deductibles, coinsurance provisions, and endorsements.

Guidelines for filling the form:

List each location separately with complete address details.

Specify construction type, year built, and updates to major systems.

Indicate protection features such as sprinklers, alarms, and distance to hydrant.

Select the correct valuation method, such as replacement cost or actual cash value.

Provide accurate building and contents limits for each location.

Attach prior loss runs and explain any significant property losses.

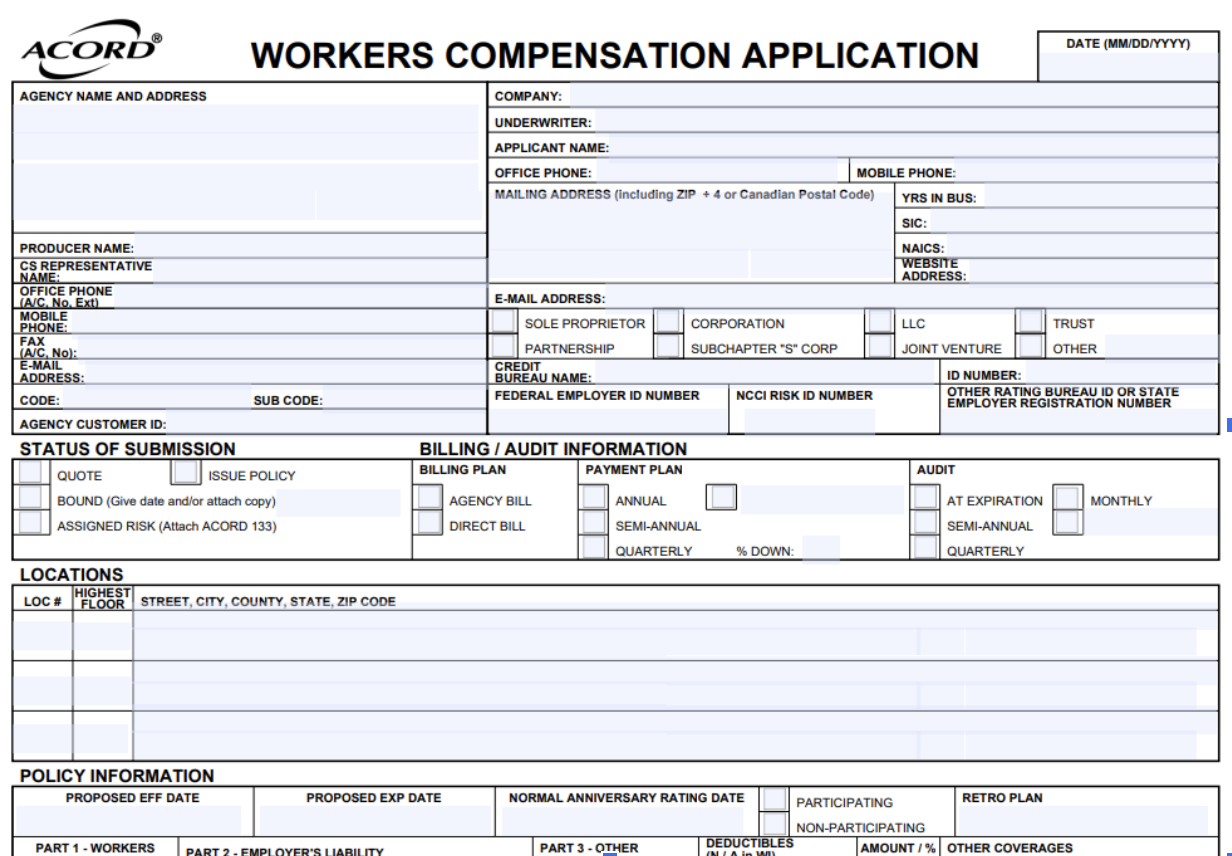

ACORD 130

The ACORD 130, Workers Compensation Application, is used to request statutory workers compensation coverage. It collects payroll estimates, employee classifications, state exposures, and prior loss information. Premium calculations are directly tied to classification codes and payroll figures reported on this form.

Because workers compensation is governed by state law, accuracy and completeness are critical. Misclassification or underreporting payroll can result in audit adjustments, penalties, or coverage disputes.

Guidelines for filling the form:

Break down payroll by class code and state of exposure.

Provide accurate estimates for the upcoming policy term.

Include experience modification factors when applicable.

Attach at least three years of currently valued loss runs.

Disclose any subcontractor relationships and certificate procedures.

Confirm compliance with state-specific filing and signature requirements.

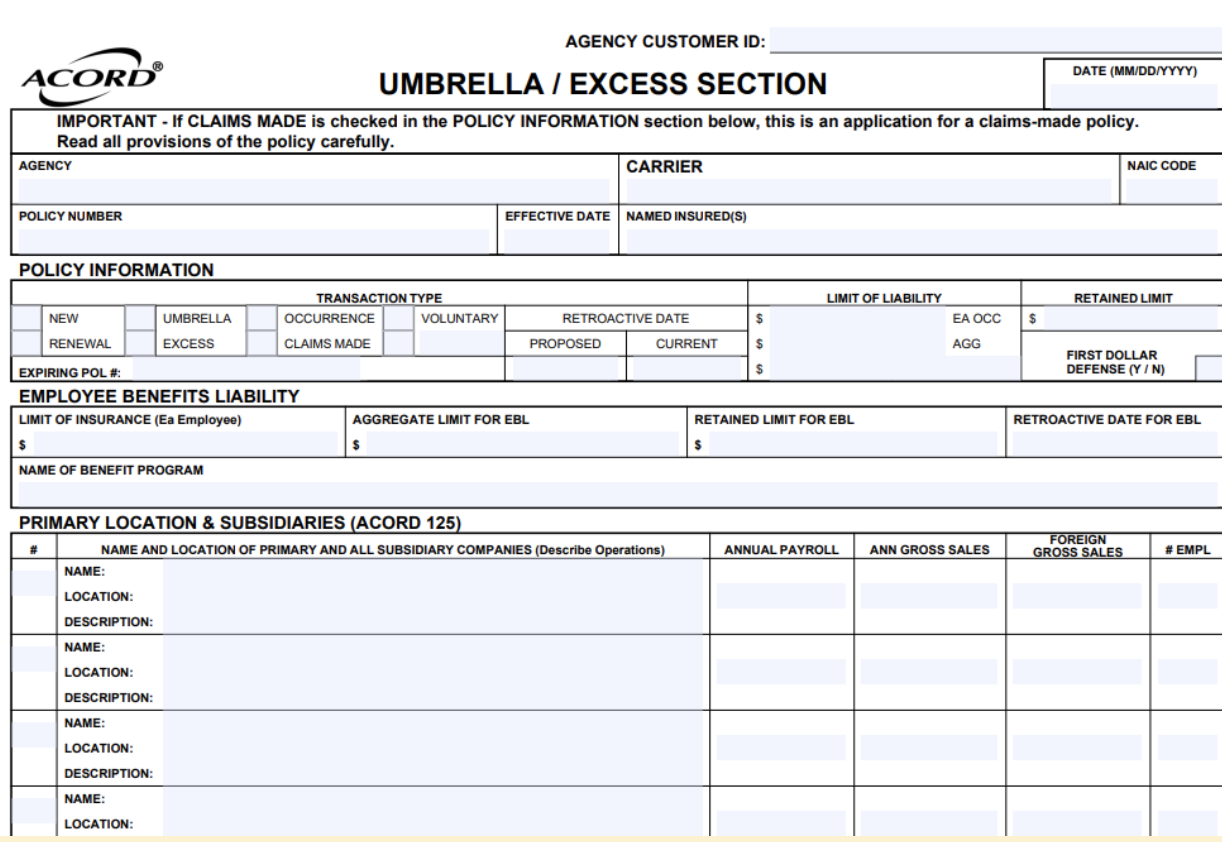

ACORD 131

The ACORD 131, Umbrella/Excess Section, supports applications for excess liability coverage above underlying primary policies. It captures total exposure data, underlying policy schedules, aggregate limits, and high-severity risk factors. Underwriters use this information to evaluate catastrophic loss potential.

The form requires a schedule of all underlying general liability, auto liability, and employers liability policies. Accurate limits and attachment points are essential to ensure the excess layer aligns with the primary program.

Guidelines for filling the form:

List all underlying policies with carrier names and limits.

Confirm that underlying limits meet minimum attachment requirements.

Disclose high-risk operations, products, or international exposures.

Provide consolidated revenue, payroll, and vehicle counts.

Attach updated loss runs reflecting large or catastrophic claims.

Ensure requested umbrella limits are consistent with overall risk profile.

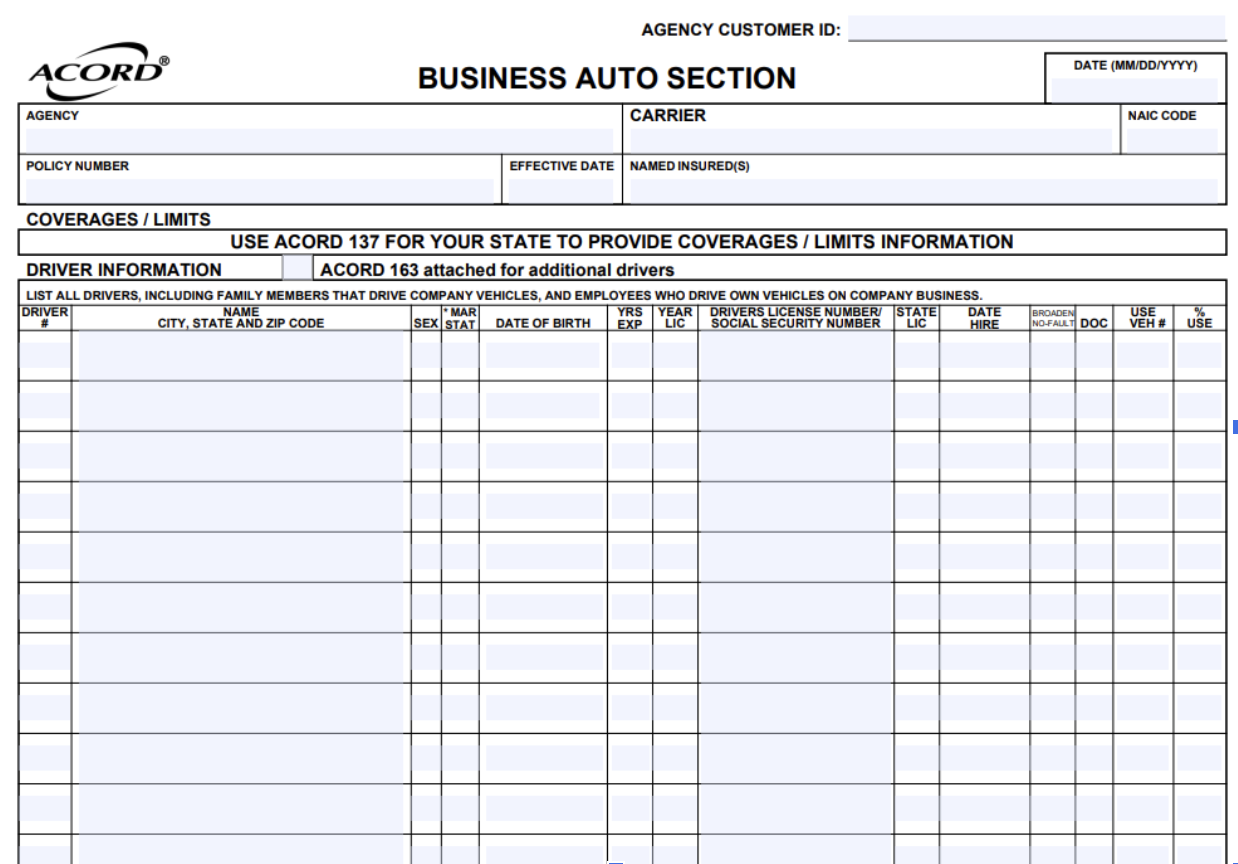

ACORD 127

The ACORD 127, Business Auto Section, is used when applying for commercial auto coverage. It records vehicle schedules, driver information, garaging locations, and radius of operation. These details affect rating, eligibility, and underwriting review.

Each vehicle must be listed with identifying information, including VIN, year, make, and model. Driver data, including license numbers and violation history, supports risk assessment and pricing decisions.

Guidelines for filling the form:

Provide complete vehicle schedules with accurate VINs.

Identify vehicle use categories and operating radius.

List all drivers and disclose accidents or violations.

Confirm garaging addresses for each vehicle.

Indicate requested coverages such as liability, physical damage, and hired auto.

Review consistency between fleet size, revenue, and operational description.

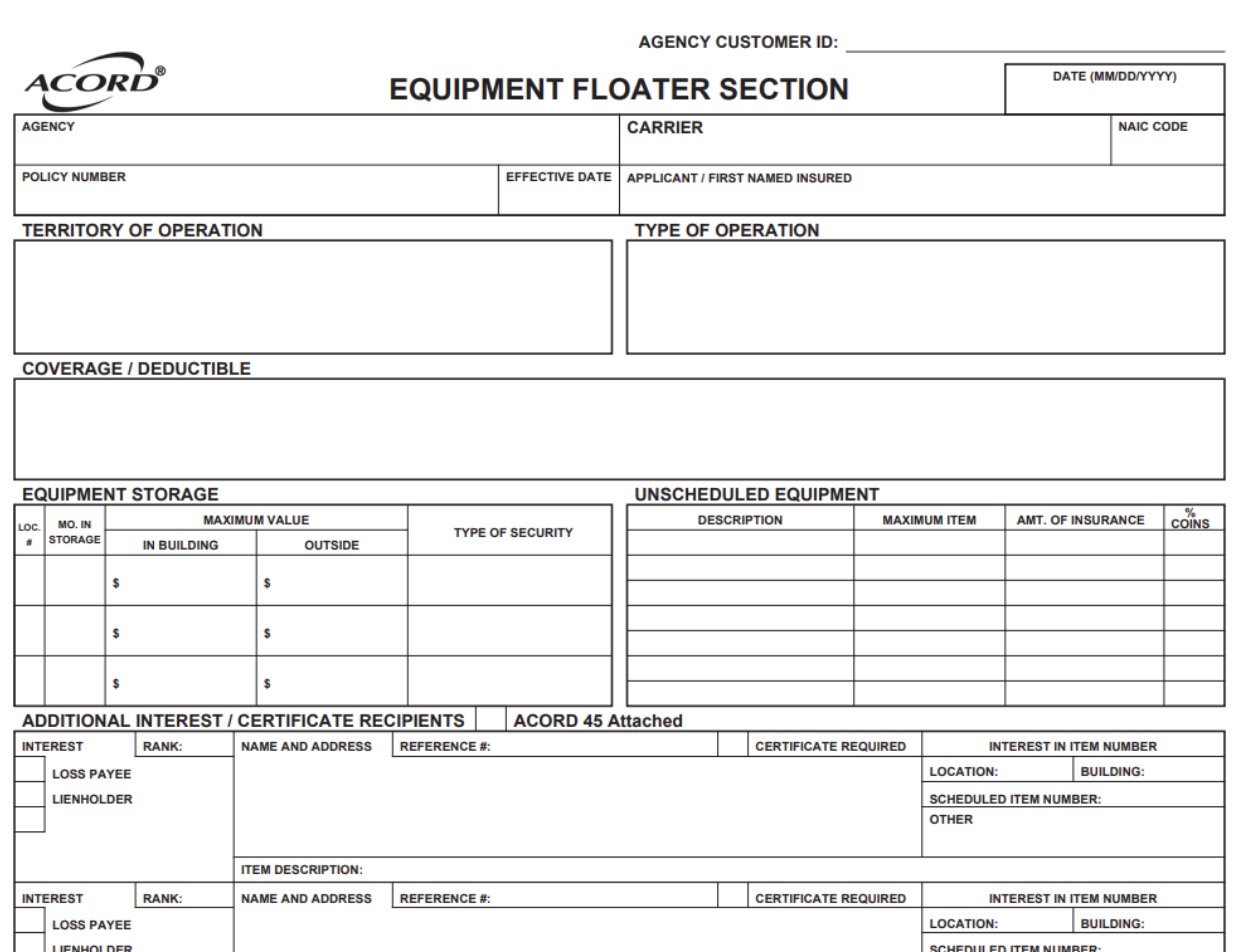

ACORD 146

The ACORD 146, Equipment Floater Section, is designed to insure mobile equipment not covered under standard property or auto policies. It applies to items such as contractor equipment, tools, and machinery that move between job sites. The form schedules each item individually with its value and description.

Because equipment is mobile and exposed to theft and damage, underwriters evaluate security, storage, and usage patterns. Accurate equipment schedules help prevent underinsurance and reduce disputes at the time of loss.

Guidelines for filling the form:

List each item with make, model, serial number, and value.

Use current replacement values rather than outdated purchase prices.

Indicate primary storage locations and security measures.

Describe how and where the equipment is used.

Disclose prior equipment losses and preventive controls.

Ensure total scheduled values align with requested policy limits.

Key Use Cases of ACORD Forms

ACORD forms are used across the insurance lifecycle, from proving coverage to submitting and reviewing risk data. Because they follow a standardized structure, they support consistent documentation, underwriting analysis, and system-driven workflows. The most common use cases include:

Certificates of insurance for business contracts: The ACORD 25 is issued to third parties as proof of liability coverage. It summarizes policy limits, effective dates, and insurer details, allowing contracts, leases, and projects to proceed once insurance requirements are verified.

Insurance applications and underwriting submissions: Forms such as ACORD 125, 130, and 140 capture structured data on operations, payroll, property, and loss history. Agents use them to submit complete applications to multiple carriers, enabling quoting, eligibility review, and premium calculation.

Risk submission and underwriting review: Underwriters rely on ACORD forms to evaluate exposures, prior claims, and safety controls in a consistent format. Detailed sections, including property and auto schedules, support pricing decisions and coverage structuring.

System integration and automation: ACORD data formats are integrated into agency and carrier systems to automate intake, validation, policy issuance, and compliance tracking. Standardized fields support electronic submission, rule-based checks, and audit trails.

Analyzing ACORD Forms with AI

AI systems can analyze ACORD forms to automate compliance checks, underwriting validation, and document review. Because ACORD forms follow a standardized structure, they are well suited for automated parsing and rule-based evaluation.

Compliance Guidance

One practical use case involves treating the ACORD 25 (Certificate of Liability Insurance) as an input document that must be reviewed for compliance with specific contractual or carrier requirements. Instead of manually reviewing each certificate, an AI agent can extract key fields and validate them against predefined rules.

For example, the system can perform limit checks by verifying that coverage amounts meet required thresholds. If a contract requires general liability per occurrence limits of at least $1,000,000, the AI compares the stated limit on the ACORD 25 to that requirement and flags any deficiency.

Lookups and Controls

AI can also perform carrier rating lookups. If the certificate lists an insurance carrier but does not include its financial strength rating, the system can query trusted sources such as AM Best, NAIC databases, or internal rating repositories. It then confirms whether the carrier meets minimum rating standards and flags non-compliant carriers.

Policy date validation is another common control. The AI reviews effective and expiration dates to confirm that coverage falls within the required policy window for a transaction, lease, or contract. Expired or soon-to-expire policies can be automatically identified before approval.

Endorsements and additional insured status can also be analyzed. The system scans for language indicating that required endorsements are included or that specific parties are listed as additional insureds. If required wording is missing, the document is flagged for review.

Report Generation

After completing its analysis, the AI agent can generate a structured compliance report. This report may be attached as a PDF and accompanied by an email summary sent to the appropriate reviewer. The result is faster turnaround, consistent enforcement of insurance requirements, and a documented audit trail.

In addition to reviewing incoming certificates, AI can also support outbound workflows. For example, structured data from ACORD applications can be validated before submission to carriers, ensuring completeness and reducing underwriting back-and-forth. Together, these use cases show how AI enhances both compliance monitoring and submission quality across the ACORD ecosystem.

Analyze ACORD forms with Kolena AI, get started today!

Best Practices for Working with ACORD Forms

1. Always Use Current, Mandatory Form Editions

Regulatory changes and carrier guidelines continually impact the required content and format of ACORD forms. Using outdated forms can result in rejection of applications, claims delays, or compliance violations. Agencies should routinely verify that the latest authorized editions—bearing ACORD copyright—are in use for every transaction. Checking carrier and ACORD updates is a key step in every operational workflow.

Failing to maintain current forms exposes agencies to regulatory sanctions and market conduct risk. Carriers may refuse to process non-compliant submissions, and courts may question coverage intent if outdated documents are referenced during disputes or audits. Storing templates in a controlled digital repository, updated via licensed channels, is an effective method for mitigating these risks.

2. Prefill Once and Propagate Across Related Forms

Re-entering duplicate data across multiple ACORD forms invites errors and wastes time. Agencies should adopt systems and workflows that allow for single-entry data capture—especially for sections like named insured details, business addresses, and broker contacts. This information can then be automatically propagated to all associated forms in a transaction set, whether it’s a new business submission, policy change, or renewal.

Prefilling reduces simple handwriting or keystroke mistakes, enhances client satisfaction, and supports more consistent insurance documentation. When forms are linked, agencies can better track client histories, accelerate renewals, and streamline re-marketing to alternative carriers without redundant effort.

3. Validate Against Carrier-Specific Underwriting Rules

While ACORD forms provide an industry standard, every insurer may have its own underwriting requirements, eligibility guidelines, and documentation thresholds. Before submitting forms, agents should run completed applications through rule validation engines that check for carrier-specific differences: minimum premiums, required attachments, or specialized questions.

This vetting step helps reduce unnecessary correspondence and cycle time between agency and carrier underwriting teams. Automated validation tools can alert agents to incomplete sections, conflicting answers, or missing signatures before forms are sent—improving acceptance rates and supporting higher policy issue volumes.

4. Restrict Certificate Issuance Authority and Log Every Event

Issuing ACORD 25 certificates confers responsibility and risk. Agencies should enforce strict controls over who is authorized to generate, modify, or distribute certificates of insurance. Access restrictions, user-level permissions, and mandatory approvals reduce the risk of erroneous or fraudulent certificate issuance.

Maintaining detailed logs of every certificate action—including requests, approvals, edits, and distributions—is essential for regulatory compliance and audit defense. Digital logs provide transparency, enable forensic review in the event of disputes, and help identify and correct process deficiencies quickly.

5. Maintain Proof of Licensing and EULA Compliance

Producing and distributing ACORD forms is a licensed activity. Agencies must maintain current proof of licensing from both ACORD and any carriers that require authorization to use branded forms. Documentation should address end-user license agreements (EULAs) and be readily available for inspection during audits or market conduct reviews.

Failure to maintain proper licensing can result in fines, credential suspensions, or legal disputes. Automated compliance modules within agency management systems can help track license expirations, EULA acceptance, and user entitlements for form access. Proactive management of these records ensures continuous legal operation and protects against involuntary service interruption.

6. Train for State‑Specific Prohibitions and Nuances

Many states dictate specific requirements or prohibitions on ACORD form usage. For example, some jurisdictions restrict modification of certificate language, limit the use of certain forms (like evidence of property insurance), or require unique consumer disclosures. Agency staff should be actively trained and updated on state-specific regulations that affect form completion and submission.

Regular compliance training reduces inadvertent violations and supports more reliable insurance servicing across state lines. Documenting staff training and periodic knowledge checks provides defensible evidence for regulators and underscores the agency’s commitment to doing business with integrity and accuracy.

Automatically Analyzing ACORD Forms with Kolena AI

Kolena AI enables insurance teams to automatically analyze ACORD forms—especially high-volume documents like the ACORD 25 (Certificate of Liability Insurance)—with speed and precision. In real-world deployments, the ACORD form is treated as an input that must be validated against carrier guidelines or contractual requirements. Kolena’s AI agent extracts key fields and performs structured checks such as verifying coverage limits against thresholds (e.g., general liability per occurrence ≥ $1,000,000), validating policy effective and expiration dates against required windows, and detecting endorsements or additional insured language. It can also enrich incomplete data by performing carrier rating lookups through trusted sources like AM Best, NAIC, or internal databases, ensuring compliance even when the original document is missing critical information.

Beyond validation, Kolena automates the entire workflow around ACORD form processing. Once analysis is complete, the AI generates a structured compliance report—typically delivered as a PDF with a summarized email notification—and routes it to the appropriate stakeholder for review or approval. This eliminates manual back-and-forth, reduces processing time, and ensures consistent enforcement of underwriting and contractual requirements. The same platform can be extended to other ACORD forms and adjacent workflows mentioned throughout this guide, enabling insurers, brokers, and risk teams to scale document analysis while maintaining accuracy, auditability, and operational efficiency.