What is ACORD 25 (Certificate of Liability Insurance)?

An ACORD 25 (Certificate of Liability Insurance) is a standardized form used across the insurance industry to provide proof that a business or individual carries active liability insurance. It acts as a quick snapshot of your active policy limits and coverages.

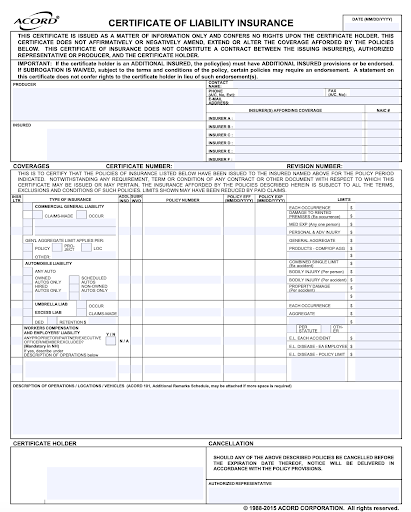

Key information included:

Named insured: The specific business or individual covered by the policy.

Insurance provider: The issuing insurance company.

Policy number & dates: The active policy numbers, as well as the effective and expiration dates.

Types of coverage: Listings for General Liability, Commercial Auto, Umbrella/Excess, and Workers' Compensation policies.

Coverage limits: The exact dollar amounts for maximum payouts (e.g., per occurrence, aggregate limits).

Who requests it? You will typically be asked for an ACORD 25 by clients, general contractors, property managers, or event venues when you enter into a business contract. It verifies that you have the required protection in place in case of bodily injury, property damage, or other liability claims during a project.

How to get an ACORD 25? You cannot fill this out yourself. To obtain an official ACORD 25, you must contact your insurance agent, broker, or carrier. They will review your active coverage and generate the verified certificate to send directly to you or the requesting party.

This is part of a series of articles about ACORD forms

Try our AI-powered loss run analysis tool

Experience the power of AI automation with your own documents. Upload a loss run report PDF. Receive a loss run spreadsheet for claims analysis generated by AI within moments.

Go To AI Loss Run Analysis ToolWhat Is the ACORD 25 Form Used For?

Proving Business Liability Insurance

The ACORD 25 form is used to confirm that a business maintains active liability insurance coverage. When engaging in commercial transactions, businesses are often required to provide evidence of insurance to partners, vendors, or clients. This certificate simplifies that process by condensing policy details, such as the type and amount of coverage, into a single document. It reassures all parties that financial protections are in place if a liability claim arises during business activities.

Relying on the ACORD 25 form reduces misunderstandings and eliminates the need to share full insurance policies, which may be lengthy and confidential. Instead, stakeholders can verify coverage details and ensure compliance with contract requirements. This verification is especially important in industries where liability risks are significant, such as construction, manufacturing, and professional services. In these cases, the ACORD 25 is an administrative tool that supports business interactions and reduces risk for all involved parties.

Vendor and Contractor Compliance

For organizations that rely on vendors or independent contractors, the ACORD 25 form helps enforce insurance compliance. Many companies require third-party vendors and contractors to carry specific types and levels of liability insurance before they can begin work. By collecting ACORD 25 certificates from these parties, businesses can confirm that all subcontractors are insured, reducing exposure to liability claims resulting from their actions.

Routine collection and review of ACORD 25 certificates help organizations maintain a risk management program. If a vendor or contractor’s insurance lapses or fails to meet contractual obligations, the organization can intervene before work proceeds, avoiding disputes or uncovered losses. This approach is common in sectors such as property management, event planning, and logistics, where the actions of third parties can affect the hiring organization’s risk profile.

Lease, Loan, and Contract Requirements

Landlords, lenders, and clients commonly require businesses to provide an ACORD 25 certificate as part of lease agreements, loan approvals, or contract negotiations. This requirement ensures that the insured party has sufficient liability coverage to address potential property damage, bodily injury, or other risks that may arise from their operations. The certificate serves as a condition precedent; without it, leases may not be executed, loans may not close, and contracts may remain unsigned.

For tenants and borrowers, furnishing an ACORD 25 certificate is a routine administrative step that demonstrates compliance with contractual insurance obligations. For property owners and financial institutions, reviewing the certificate provides assurance that their interests are protected. If an incident occurs, they can confirm that the responsible party has the necessary insurance to respond to claims, limiting their financial exposure.

Construction and Professional Services

In construction, the ACORD 25 form is a standard requirement before any contractor or subcontractor sets foot on a job site. Project owners and general contractors use it to verify that all parties working on a site have appropriate liability insurance, including general liability, workers’ compensation, and sometimes additional coverages like umbrella liability. This verification process helps prevent uninsured or underinsured parties from introducing risk to the project.

Similarly, professional service providers, such as architects, engineers, consultants, and IT firms, are often asked to supply ACORD 25 certificates to clients. These certificates confirm the provider’s professional liability or errors and omissions (E&O) coverage, which is important for services that could result in financial loss due to mistakes or negligence. In both construction and professional services, the ACORD 25 supports risk management and ensures compliance with industry standards and contractual agreements.

Who Requests It?

Requests for an ACORD 25 certificate typically come from parties that have a vested interest in verifying a business’s insurance status before engaging in a professional relationship. These requestors include clients, property managers, project owners, lenders, and government agencies. Their goal is to ensure that the business they are working with maintains sufficient liability coverage to address claims or damages that might occur during work, rental, or service provision.

Contractual agreements often specify the minimum required insurance coverage, and the ACORD 25 certificate provides a way for the requesting party to verify compliance. In some industries, this request is a standard administrative step before contracts are finalized or work begins. By collecting and reviewing these certificates, the requesting entity reduces its risk exposure and ensures that all parties operate within agreed safety and legal frameworks.

Key Information Included in ACORD 25

Named Insured

The “named insured” section of the ACORD 25 identifies the individual or business entity that holds the insurance policy. This information is critical because only the named insured is covered under the terms of the policy. Accurate listing of the insured’s legal name and address is necessary to avoid disputes or coverage issues if a claim arises. Errors or omissions in this section can result in delays or denials during the claims process.

The named insured is usually the primary party responsible for fulfilling contractual obligations and maintaining coverage. For companies with subsidiaries or multiple divisions, it is important to ensure the correct entity is listed. In cases where additional insureds are required, such as project owners or landlords, this information is typically included in a separate section or via endorsement, but the named insured must always be clearly identified on the certificate.

Insurance Provider

The insurance provider, or carrier, is the company that underwrites and issues the liability policy referenced in the ACORD 25 certificate. Listing the insurance provider allows certificate holders to verify the legitimacy and financial stability of the insurer. A reputable provider increases confidence that claims will be handled according to industry standards.

It is common for the ACORD 25 form to list more than one insurance provider if multiple policies from different companies are involved. Each provider’s name and contact information should be accurate and up to date. This allows certificate holders to contact the insurer with questions, verify policy status, or report claims if necessary. The presence of a recognized insurance provider on the certificate adds credibility to the insured’s coverage.

Policy Number and Dates

The ACORD 25 form includes the policy number for each listed coverage, providing a unique identifier for the insurance policy. This number enables certificate holders to verify the policy referenced and communicate with the insurance provider in case of questions or claims. Accurate policy numbers reduce confusion and help prevent fraudulent or outdated documentation from being used to satisfy insurance requirements.

In addition to the policy number, the form specifies the effective and expiration dates of each policy. These dates indicate the period during which coverage is active. Requestors must ensure that the certificate reflects current and valid coverage, as an expired policy provides no protection. Monitoring these dates is important for ongoing compliance, especially for contracts or projects with long durations.

Types of Coverage

The ACORD 25 certificate lists the types of liability insurance carried by the insured. Typical categories include general liability, automobile liability, workers’ compensation, and umbrella or excess liability. Each type of coverage is listed separately, with corresponding policy numbers, limits, and effective dates. This structure allows certificate holders to confirm that required coverages are in place.

For specialized industries or contracts, the ACORD 25 may also indicate additional coverages such as professional liability, pollution liability, or cyber liability. The inclusion or exclusion of specific coverages can affect risk exposure for all parties. A detailed review of the coverage types listed on the certificate is necessary for compliance and risk management.

Coverage Limits

Coverage limits on the ACORD 25 form specify the maximum amount the insurer will pay for a covered claim under each policy. These limits are typically broken down by type of coverage, such as per occurrence and aggregate limits for general liability, or combined single limits for auto liability. The certificate holder must verify that these limits meet contractual or regulatory requirements before accepting the certificate.

Failure to maintain adequate coverage limits can expose both the insured and the certificate holder to financial risk in the event of a claim. For this reason, contract administrators and risk managers review these limits during the certificate review process. If limits are insufficient or do not match contractual requirements, the insured may need to obtain additional coverage or endorsements before work can proceed.

Related content: Learn more about the ACORD 140 property section and how to complete it.

Learn more about ACORD 125.

ACORD 25 vs. Certificate of Insurance

Many people use the terms “ACORD 25” and “certificate of insurance (COI)” interchangeably, but they are not the same.

A certificate of insurance is a general term for any document that summarizes insurance coverage and provides proof that a policy exists.

ACORD 25 is a specific standardized certificate of insurance form developed by ACORD for liability insurance. In other words, every ACORD 25 is a certificate of insurance, but not every certificate of insurance is an ACORD 25.

Another important distinction is that the ACORD 25 form only summarizes policy information and does not modify the insurance contract. It does not grant coverage, create additional insured status, or change policy limits unless supported by the underlying policy and endorsements. Certificate holders should rely on the actual insurance policy and endorsements for definitive coverage terms.

How to Get an ACORD 25

Businesses obtain an ACORD 25 certificate from their insurance agent, broker, or insurance carrier. Once liability insurance is in place, the insured can request a certificate identifying the party that requires proof of coverage. In many cases, agents can generate and deliver the certificate electronically within a short period.

Before issuing the certificate, the insurance representative verifies the policy details, including coverage types, limits, policy numbers, and effective dates. The certificate holder’s name and address are then added to the document, along with any required references to contracts, projects, or locations. Accuracy is important because incorrect information can result in rejected certificates and delays in business transactions.

If a contract requires additional insured status, waiver of subrogation, or other special insurance provisions, the business may need policy endorsements in addition to the ACORD 25 certificate. The certificate itself does not provide these rights unless they already exist within the policy. Contract requirements should be reviewed carefully before requesting the certificate.

Manual ACORD 25 Review: Common Operational Challenges

High Document Volume

Organizations that work with large numbers of vendors, subcontractors, tenants, or service providers often receive hundreds or thousands of ACORD 25 certificates each year. Reviewing each certificate manually can create significant administrative workload, especially when documents arrive in different formats and at different times. Staff must open each certificate, locate key information, and compare it against contractual insurance requirements.

As document volume increases, review backlogs become more common. Delays in processing certificates can slow onboarding, contract execution, and project approvals. High volumes also increase the likelihood of human error, making it difficult for risk management and compliance teams to maintain consistent oversight across certificate submissions.

Repetitive Field Verification

Manual ACORD 25 review requires personnel to verify the same set of fields, including insured names, policy numbers, coverage types, limits, effective dates, and certificate holder information. While each review follows a similar process, employees must inspect every certificate to ensure the information matches contractual requirements and internal standards.

This repetitive work is time-consuming and can lead to fatigue-related errors. A reviewer may overlook an expired policy, incorrect coverage limit, or missing endorsement after processing many certificates. Even small mistakes can create compliance gaps that expose organizations to financial and legal risks if a claim occurs.

Expiration and Renewal Tracking

Insurance policies listed on ACORD 25 certificates have expiration dates that must be monitored throughout the life of a contract, lease, or project. Many organizations maintain spreadsheets or manual tracking systems to record renewal deadlines and follow up with vendors when updated certificates are required. As the number of certificates grows, keeping these records current becomes more difficult.

Missed renewals can result in vendors or contractors continuing work without valid insurance coverage. This creates risk and may place the organization in violation of its contractual or regulatory requirements. Effective expiration tracking requires ongoing monitoring, timely notifications, and consistent follow-up to ensure that replacement certificates are received before coverage lapses.

How AI Can Help with ACORD 25 Certificate Reviews

Reviewing certificates of insurance often involves extracting information from documents, validating coverage details, and monitoring compliance requirements. AI can automate many of these tasks, reducing manual effort and improving consistency.

Automatically extract key certificate data: AI can read ACORD 25 forms and capture information such as insured names, insurance carriers, policy numbers, coverage types, limits, effective dates, expiration dates, and certificate holder details.

Validate coverage against requirements: Insurance requirements often vary by contract, vendor type, project, or location. AI can compare certificate information against predefined requirements and identify missing coverages, insufficient limits, expired policies, or other compliance issues.

Review supporting documents: AI can analyze endorsements, contracts, lease agreements, and other insurance-related documents, and cross-reference information to identify inconsistencies or missing requirements.

Track expirations and renewals: AI-powered workflows can monitor policy expiration dates and flag certificates that require renewal.

Improve review speed and consistency: AI applies the same review rules to every certificate, helping organizations process large numbers of documents while maintaining consistent standards.

Support auditability and compliance: AI systems can maintain records of extracted data, validation results, and review decisions.

By automating data extraction, validation, monitoring, and document review, AI can help organizations manage certificate of insurance workflows while reducing administrative workload and compliance risk.

Related content: Explore how AI is transforming insurance operations.

How to Automate ACORD 25 Certificate Reviews with Kolena

Manually reviewing ACORD 25 certificates—checking insured names, policy numbers, coverage types, limits, and expiration dates against contract requirements—is slow, repetitive, and prone to error at scale. Kolena's AI for Insurance automates the document-heavy work behind certificate and underwriting reviews, extracting and validating data from ACORD forms, loss runs, and compliance documents so your team can focus on decisions instead of data entry.

Key capabilities of Kolena:

Automated document extraction: Ingest ACORD forms, loss runs, policy binders, and compliance documents, and automatically extract key values—insured names, carriers, policy numbers, coverage types, limits, and dates—with 99%+ accuracy.

Validation and anomaly detection: Compare extracted certificate data against your requirements to flag missing coverages, insufficient limits, expired policies, and other compliance anomalies.

Fraud and compliance monitoring: Analyze policy and applicant data to surface inconsistencies and reduce missed compliance issues, with audit-ready, regulator-compliant outputs.

Standardized, consistent review: Normalize formats and apply the same review rules across every carrier and document, cutting review time from weeks to minutes.

Enterprise-ready and secure: SOC 2 Type II certified and HIPAA-compliant, deployable in hours with no complex IT project, and built to scale as your portfolio grows.

Ready to cut manual certificate review from weeks to minutes? Learn more about Kolena's AI for Insurance.